November 2023 Market Summary

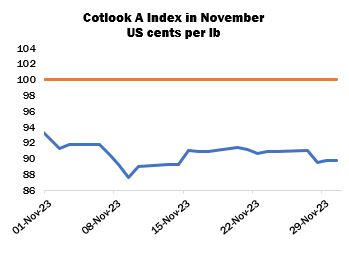

New York futures traded within a lower range in November than the previous month: on November 7, the March contract closed below 80.00 cents per lb for the first time since July and did so in a further seven sessions before the month’s end. World prices followed, and the Cotlook A Index declined from its high, recorded at the beginning of the period (92.60 cents per lb), to reach a low of 87.55 on November 9 and fluctuate around 90.00 thereafter. Overall, fluctuations were narrow and the market lacked a clear direction.

Meanwhile, China’s Zhengzhou cotton futures saw a downward trend again during November, trading below 16,000 yuan per tonne and reaching a low of 14,950 yuan toward the end of the month.

Despite lower futures and offering rates, trade in the physical market remained subdued. Slow downstream demand was again a key barrier to business for many spinners, as well as ongoing difficulties in opening Letters of Credit in countries such as Bangladesh and Pakistan. Thus, enquiries remained sporadic and largely limited to those with pressing requirements. Some volumes of Brazilian or US recaps moved, as well as lower-quality discounted lots and supplies available afloat or for prompt shipment.

In China, procurement from the international market slowed as the gap between domestic and world prices narrowed. An ample local supply – the domestic crop has been steadily arriving at gins, while imported lots consigned at ports were also available –affected sentiment. The country nonetheless accounted for 58 percent of the 2023/24 upland export registrations as reported by the USDA between October 26 and November 23 (738,100 running bales out of a total of 1,263,400), but Vietnam replaced China as the largest destination in the last report of that period. Purchasing by the State Reserve also continued to be a focus of discussion – as mentioned in October’s summary, the proportion of buying versus selling this year is estimated to be about balanced. Although stocks may not yet be at an optimal level (from Beijing’s perspective), it would seem that for now at least, import buying may have paused.

The Reserve sales programme was concluded on November 14. The auction series was launched with the objective of cooling local prices and ensuring supply, aims which were sufficiently met. The total volume of cotton sold amounted to almost 885,000 tonnes, including 70 percent imported cotton and representing 72 percent of that offered. The average price paid was 17,274 yuan per tonne, up from 15,896 yuan last year.

In the United States, the Department of Agriculture increased its domestic production figure from 12.8 to 13.1 million bales (480 lbs) as lower output in Texas was more than offset by improvements in yield elsewhere. By November 26, 83 percent of the crop had been harvested nationwide, on a par with last year but slightly above the five-year average.

Elsewhere, the Cotton Association of India published its latest 2023/24 balance sheet, leaving most figures unchanged save for a 100,000-bale reduction to output in Haryana, bringing the nationwide total forecast to 29.41 million bales (170 kgs) and the season’s closing stock to two million. Meanwhile, the Committee on Cotton Production and Consumption issued its first estimations for the season, placing output at 31.66 million bales and consumption at 31 million. The figures suggest that India may not be a major exporter to the international market during the 2023/24 season. The Cotton Corporation of India reported arrivals by the end of November at five million bales.

In Pakistan, picking is complete and deliveries to gins have continued. The arrivals tally as of November 30 according to the Pakistan Cotton Ginners Association stood at almost 7.8 million lint equivalent bales, exceeding the final total for the 2021/22 season. Unusually, the volume in Sindh has exceeded that in Punjab, a trend partially attributed to a higher level of unreported business and pest attacks in the latter province, in contrast to higher yields in the former.

This season’s production in Brazil has been forecast at 3.3 million tonnes by ABRAPA, while CONAB’s estimate stood at 3.04 million. By the end of the month, sowing had begun in Bahia, but little had taken place in Mato Grosso. Late rains and the presence of El Niño have stimulated discussions around the impact on the crop, and the possibility of planting cotton as a first crop (safra) in replacement of early soybeans. In Argentina, rains were welcomed, and sowing has advanced where moisture has allowed. An increase in area may be in prospect, but field work remained in its early stages.

Cotton Outlook’s November supply and demand review saw a reduction of the global raw cotton output forecast for 2023/24 of 519,000 tonnes to 24.08 million tonnes. The downward adjustment is attributed to China, India, Turkey and Australia, partially offset by increases for the US and Pakistan. Our world consumption estimates for both the current and previous seasons were raised slightly, owing to higher figures in Turkey. The margin by which output is expected to exceed consumption in 2023/24 has narrowed to 188,000 tonnes.