August 2023 Market Summary

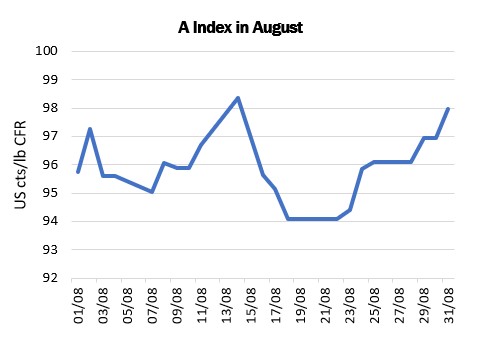

The movement of the Cotlook A Index during August was characterised by two separate spikes. On each occasion, under the lead of New York futures, the Index approached the dollar mark – a threshold not crossed since early March – but both times fell short.

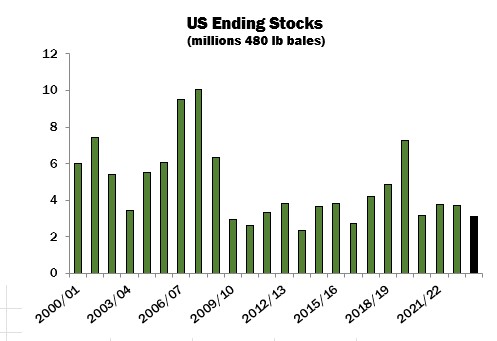

Uncertainty with regard to the United States 2023/24 crop was a major influence on market sentiment throughout the month. On August 11, the Department of Agriculture released its first state-by-state production forecast. Although a reduction had been anticipated, the size of the adjustment took the market by surprise. Projected output was decreased from the 16.5 million bales (480 lb) indicated in July, to below 14 million (Cotton Outlook’s estimate, also lowered in August, is equivalent to just below 14.7 million bales). The Department projected higher abandonment and lower yields in Texas. Exceptionally high temperatures and mainly dry conditions have taken a toll on cotton the West Texas growing region, which typically accounts for about half US cotton area. The August WASDE report lowered the season’s expected US ending stocks from 3.8 to 3.1 million bales.

The attritional stress experienced on the Texas Plains was not the only weather event to threaten the US cotton belt. Early in the month, Pima fields escaped damage when Tropical Storm Hilary veered east of the San Joaquin valley. That weather system was closely followed by TS Harold, which arrived in South Texas – but after the bulk of that region’s crop (the earliest in the US) had been picked. Finally, at the end of the month, Hurricane Idalia wreaked havoc in Florida and the Carolinas, but a preliminary assessment is that the impact on the Southeast crop has been limited. Be that as it may, these events have been consistent with expectations of an active hurricane season, one that is of course far from over.

Another potentially significant climatic anomaly is the exceptionally dry month of August experienced by India. The effect on yields in the more vulnerable cotton-producing states has yet to become clear. Meanwhile, with sowing in its final stages, it seems likely that cotton area will decline slightly from that attained last season.

Optimism in Pakistan was broadly maintained. The country has been spared the torrential rainfall that brought devastation to parts of the country a year ago. With an exceptional volume of seed cotton already delivered by mid-August (reflecting the scale of early plantings) and the bulk of the crop approaching maturity, most local forecasts continue to indicate a strong recovery of output.

As for the African Franc Zone, data disclosed during August suggest that the area sown to cotton has fallen short of intentions in several countries. Production forecasts have accordingly been revised downward.

The effect of these various adjustments is that by the end of August, and for the first time since the initial figures were advanced in February of this year, Cotton Outlook’s forecast of global raw cotton production in 2023/24 shows a decrease (albeit a modest one) in comparison to the estimate for 2022/23.

Even so, our latest estimates suggest an increase in world stocks of over a million tonnes by the end of the current marketing year. The weakness of the demand side of the world market has for many months been its defining feature. The lacklustre trading conditions reported by virtually all major raw cotton import markets will be all too familiar to readers of Cotton Outlook. Poor downstream demand for textiles and garments has led to stagnant yarn sales. In response, most spinners have remained wedded to a hand-to-mouth policy in respect of raw cotton purchasing. A consistent complaint has been that current raw cotton replacement costs represent a loss-making proposition in the absence of any improvement in yarn prices.

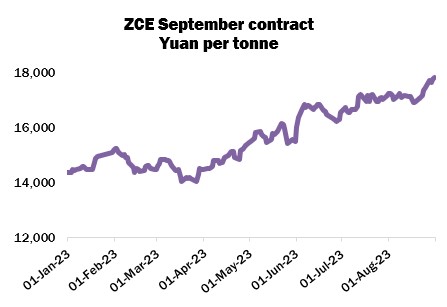

For some months, the principal source of import demand has been China, as private and state-owned trading houses have taken advantage of a favourable relationship between local and international prices to purchase significant volumes of US and Brazilian cotton in particular. Buying interest has also been fuelled by the perception that local stocks are tightening in advance of the arrival of the domestic 2023/24 crop and uncertainty with regard to the size of that crop. Zhengzhou cotton futures continued to show strength during the month under review. The spot contract settled at a new high on August 31, having gained almost four percent during the period and over 24 percent since the turn of the year.

In an endeavour to calm the bullish mood of the domestic market, in July the authorities announced that a State Reserve auction series would be launched and that a discretionary import quota amounting to 750,000 tonnes would be established. In both cases, participation would be confined to spinners. Sales from the State Reserve commenced on July 31, since when daily catalogues have sold out every day. By the end of August, the volume purchased amounted to more than 250,000 tonnes, comprising mainly imported cotton purchased between 2018 and 2022, as well as a smaller volume of Xinjiang cotton acquired in 2019.

Toward the end of the month, some signs of healthier raw cotton import demand began at last to be observed in markets outside China. In Bangladesh most notably, the flow of ready-made garment export orders showed a long-awaited improvement, as did the volume of yarn sales and the prices obtained. The upturn was not as visible in other markets but raised hopes that a more general revival of spinners’ fortunes may be in the offing.