February 2023 Market Summary

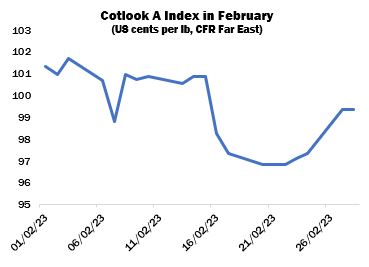

International cotton prices, as measured by the Cotlook A Index, continued to fluctuate either side of the dollar mark in February, under the lead of movements in the nearby ICE futures market. Barring a few sharp movements, daily changes in New York were fairly modest, and prices remained within the range that has been in force since early November. The A Index began the month at its high point of 101.35 US cents per lb and fell to a nadir of 96.85 cents late in the period, before regaining some ground to settle two cents below its opening level.

The slightly more optimistic market sentiment that emerged in January was dampened somewhat by a realisation as the month wore on that mill demand appeared not to have revived to the extent expected by some observers. Business remained focused on cotton for nearby delivery, often with a requirement that sellers make concessions on their price ideas. In Bangladesh and Pakistan, difficulties in opening Letters of Credit persisted and so business to those destinations was affected. However, late in February it was reported that Pakistan had been granted a credit facility amounting to around US$700,000,000 by the China Development Bank, while talks were also ongoing with the International Monetary Fund to secure further funding. In the latter regard, considerable reforms have been required, including an increase of energy prices that has impacted the domestic textiles sector.

Vietnam mills were again among the more active buyers during February, with spinners entering the market when ICE futures fell to the low 80s cents per lb (allowing for a landed price below one dollar). Some import demand was also noted in China, predominantly from state-owned entities, facilitated by a convergence of local and international prices mid-month.

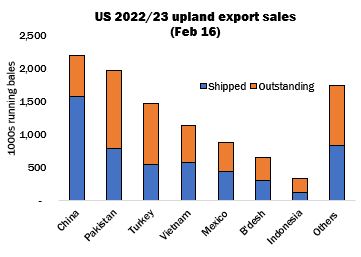

Meanwhile in Turkey, humanitarian efforts eclipsed all other factors following the series of earthquakes that caused huge loss of life and widespread destruction of infrastructure across much of the southeast of the country, where the majority of the spinning and textiles industry is located. In the aftermath, merchants were asked to pause cotton shipments for up to 45 days, pending a clearer assessment of the situation, and cargo en route to that destination was diverted to alternative ports. In the last US export report released during February, which recorded the second weekly marketing year high of the period in view (more of which below), the volume of unshipped US cotton destined to Turkey was placed at 63 percent of that country’s total commitment equivalent to over 1.5 million statistical bales (480 lbs).

The US export reports issued during the month in question brought the total export commitment to within 10 percent of USDA’s projection for the season (12 million bales). The major destination for US cotton exports was still China (almost 2.3 million), largely by dint of unshipped commitments carried over from last season, and new purchases have featured over recent weeks, following a lengthy absence. In second place was Pakistan with slightly over two million bales, around 60 percent of which remained to be shipped.

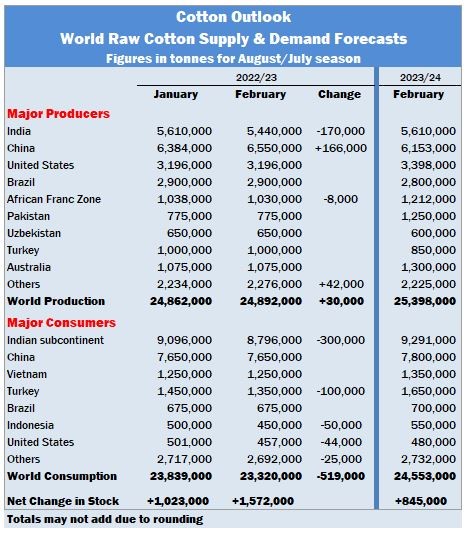

Cotlook’s initial estimates for production and consumption next season were published on February 23. As always, these early projections are accompanied by strong caveats, given that sowing of cotton has yet to begin in the Northern Hemisphere and forecasts of consumption concern a period that will not start for several months.

At this early stage, our first tentative forecasts place world production at slightly below 25.4 million tonnes, representing an increase of two percent on the previous season. While the historically high level of prices would normally encourage enthusiasm for cotton among farmers, the sharp rise in production costs (including higher prices for pesticides and fertiliser), as well as the relatively good returns obtainable from competing crops, have resulted in an expectation that planted area will remain about steady in 2023/24. The modest increase in production is therefore predicated on the assumption that weather conditions will be more benign than in the current season, which saw extreme drought in parts of the United States, flooding in Pakistan and severe pest infestations in West Africa.

As for consumption, the most recent forecasts of global macro-economic performance indicate a return to growth in 2024. While any attempt to predict global raw cotton consumption in the coming 18-month period is as always fraught with difficulty, a cautious optimism has informed Cotlook’s initial number, which placed at 24,553,000 tonnes would represent an increase of more than five percent in relation to the 2022/23 season.

As a result of the above adjustments, world stocks are forecast to increase by 845,000 tonnes at the end of 2023/24, which added to the figure for the current season of 1,572,000 tonnes, would amount to an addition to global stock levels of more than 2.4 million tonnes over the two-season period.