September 2023 Market Summary

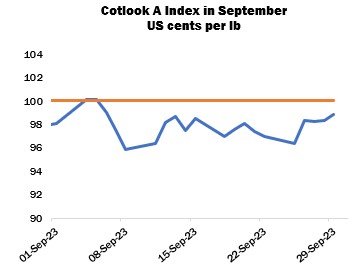

The Cotlook A Index remained above 95.00 cents per lb in September, peaking early in the month at just over a dollar, a level not reached since early March. Fluctuations were minimal thereafter, following a largely directionless and range-bound pattern of trade in New York futures.

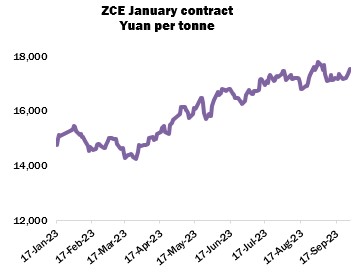

Zhengzhou cotton futures remained firm over the month. The January contract reached a record high settlement on the first day and subsequent declines were relatively modest, keeping the lead month above 17,000 yuan per tonne. The last few days of September saw a moderate uptick as the week-long national holiday approached.

The strength of ICE futures tended to stifle mill demand in the physical market. In many consuming countries, spinners continued to cover in the familiar hand-to-mouth pattern observed for some time as downstream demand generally remained poor. More positive reports were again received from Bangladesh, although towards the end of the month, the flow of garment export orders slowed somewhat, and yarn values that had risen considerably suffered a setback. Hopes that the improvement in downstream orders for textiles and apparel would extend across other major spinning centres in the Far East and South Asia were largely disappointed. Demand for raw cotton in Vietnam and Indonesia remained lacklustre, while Turkey and Pakistan showed few signs of life as far as import enquiries were concerned.

Traders and mills in China, however, were reported to be purchasing from the international market – including Australian cotton, indicating a further easing of the ‘soft ban’ that reduced imports from that origin for over two years. Brazilian supplies also continued to be in demand on the grounds of price and availability, although congestion at ports caused some logistical difficulties.

State Reserve sales, launched at the end of July in a bid to control the upward momentum of the local market, continued throughout September and the volume offered on a daily basis was increased to 20,000 tonnes. By the end of the month over 585,000 tonnes had been sold, or 90 percent of the volume offered. Daily proportions sold after September 11 (before which daily sell-outs were recorded) varied between 61 and 98 percent. On September 27, it was announced that auctions would resume early after a shorter than usual break for the Golden Week holiday and would thereafter continue until further notice.

The expectation of firm seed cotton prices as competing ginners bid for the new Xinjiang crop led some market participants to believe that an extended programme could be in prospect. Observers also expressed the expectation that the authorities would at some stage return to the world market to replenish stocks according to the principle of rotation that governs the operations of the Reserve, and the potential for further substantial volumes to be disposed of during auctions in October strengthened that conjecture.

In the United States, the Department of Agriculture released its second detailed production forecast of the season, cutting its national production forecast further, from 13.99 million bales in August to 13.13 million. Some commentators were surprised by the lack of any adjustment for Texas, despite the fact that the crop condition has declined progressively. Harvesting in the state continued to expand, although the level of abandonment there is significant (36 percent) after sustained high temperatures over the summer months. Beltwide, 70 percent of the crop was rated either ‘fair’ or ‘poor to very poor’ by the end of the month.

A United States government shutdown loomed over the market until a temporary deal was signed at the eleventh hour on September 30, ensuring funding until November 17. The political uncertainty saw the country’s credit ratings downgraded by some agencies, whilst the prospect of disruption to government services and reports weighed on several markets.

Beyond the US, several Northern Hemisphere crops were affected by excessive rainfall in September. Parts of Greece were inundated by Tropical Storm Daniel, and experienced serious flooding, particularly in the cotton-growing region of Thessaly which may have lost approximately half of its crop. National output could therefore be below 200,000 tonnes this season, although estimates are at this stage highly tentative.

Exceptionally dry conditions in India during August were replaced by late, heavy rains across central and southern parts of the country as the Monsoon system began to withdraw, thus reducing the seasonal rainfall deficit to six percent. The downpours caused disruption in some areas, but cotton was largely spared in comparison to other crops. Elsewhere in the country, precipitation was considered beneficial. However, pink bollworm infestations in the Northern Zone have threatened both the quality and quantity of cotton in the affected fields.

Meanwhile, in Pakistan untimely showers were also experienced in the month under review, reducing the quality of some arrivals. Significant whitefly attacks added further strain on the crop, particularly in Punjab, dampening earlier optimistic output forecasts. Nonetheless, arrivals thus far have been strong, but the earlier movement of the crop and the pest damage mentioned mean the pace of deliveries could slow earlier than usual.

In our September review of supply and demand, Cotton Outlook’s forecast of global raw cotton output in 2023/24 was reduced by a further 715,000 tonnes. The United States accounted for over half of the adjustment, while smaller reductions were made for India, Pakistan, and Australia, offsetting an increase for Brazil. Meanwhile, our consumption figure for the current season was almost unchanged at 24,391,000 tonnes, five percent higher than the estimate for 2022/23. The margin by which production is expected to exceed consumption in 2023/24 therefore narrowed to 307,000 tonnes.