October 2023 Market Summary

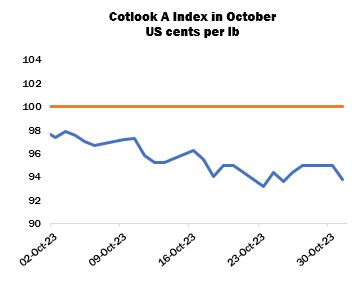

October saw fluctuations in world prices but with an overall downward trend, reflecting some erratic movements of New York futures. The Cotlook A Index declined to 93.20 cents per lb on October 23, its lowest level since July, whilst its high for the month proved to be 97.85, reached on October 3.

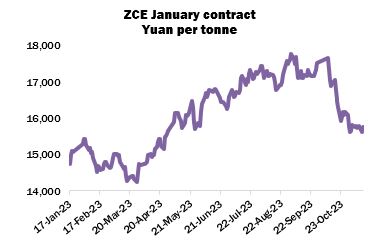

Upon return from the national week-long holiday at the start of October, Zhengzhou cotton futures also witnessed a significant decline on balance. The January contract decreased by 1,720 yuan between September 28 and October 31, ending the month at 15,800 yuan per tonne, its lowest point since the end of May.

Business in the physical market was slower than perhaps might have been expected in view of lower ICE futures and trade offering rates. Some merchants noted that the volatility had led buyers and sellers to be cautious in their approach, while continuously poor downstream demand was a more fundamental impediment to sales. Nonetheless, some enquiries and purchasing were observed, particularly when the price ideas of buyers and sellers converged at the lower end of the recent range. Mills in Bangladesh purchased Brazilian, Indian and Franc Zone supplies, whilst ex-warehouse supplies or lots available for prompt shipment were sought after to meet nearby requirements in the Far East. Import demand improved slightly in Pakistan, particularly for Brazilian and Afghan parcels, or US recaps and speciality cottons.

Purchasing from the international market also continued in China. The country accounted for over 60 percent of the 2023/24 upland export registrations recorded by the USDA between September 29 and October 26 (464,900 running bales out of 757,900 in total). Australian trade data for September showed smaller shipments to China than in the previous two months, but the figure was nonetheless notably larger than in the months prior to June as the ‘soft ban’ appeared to ease. In Brazil, congestion at ports continued to hamper shipments, but supplies from that origin remained in demand on account of their advantageous price point.

Meanwhile, State Reserve auctions continued. The daily volumes offered were maintained at around 20,000 tonnes, but the proportions sold each day varied between 11 and 98 percent. An additional 251,300 tonnes were disposed of during October, bringing the total volume sold by the end of the month to over 836,000 tonnes (77 percent of the quantity offered).

As the sales programme had been launched in a bid to ease upward pressure in the local market, the significant decline of prices in October led some market observers to anticipate that the auctions would draw to a close. However, no such confirmation from Beijing was forthcoming. At the same time, estimates of the Reserve’s possible balance sheet continued to circulate. Many observers were of the opinion that state buying and selling were more or less in balance for the year, but it remained a matter for discussion whether stocks had reached an optimal level, and at what point the authorities would withdraw from the market.

In the United States, the third detailed production forecast of the season was released by the Department of Agriculture, in which national output was reduced by 315,000 bales to 12.8 million bales. The adjustment was attributed to lower yields in Texas, offsetting gains in other states. By the end of the month, 49 percent of the crop across the belt had been harvested, and 71 percent was rated either ‘fair’ or ‘poor to very poor’. Meanwhile, the USDA adjusted its assessment of Brazilian production data, shifting ahead by a season to account for harvest timings and subsequently inflated marketing year ending stocks. As a result, a 10-million bale downward adjustment was made to world ending stocks for 2023/24.

Outside the US, harvesting continued in many Northern Hemisphere fields. Favourable weather boosted the pace of picking in Pakistan, which neared completion in many areas. According to the Pakistan Cotton Ginners Association, arrivals had reached 6.8 million lint equivalent bales by October 31, the highest total on that date since 2018. The quality of the cotton was lower than had been hoped for, a fact attributed to untimely rains and pest infestations.

The Cotton Association of India meanwhile released its first estimate of the country’s 2023/24 crop, placing output at 29.5 million bales. The figure represents a 7.5-percent decline from the organisation’s final assessment of 2022/23 production, while consumption is forecast to remain steady. The Ministry of Agriculture, however, has placed current season output higher at 31.7 million bales. Seed cotton arrivals amounted to around 2 million bales by the end of the month.

In our October supply and demand review, Cotton Outlook’s forecast of global raw cotton production in 2023/24 was reduced further, by 95,000 tonnes. The United States again accounted for the largest adjustment, followed by Australia, Chad and Cameroon, offsetting small additions for Argentina, Mali and Côte d’Ivoire. Meanwhile, our world consumption estimate for the current season was lowered by 575,000 tonnes to 23.8 million, attributed to Turkey, China, Indonesia, and the Indian subcontinent. Thus, the margin by which production is projected to exceed consumption widened to 787,000 tonnes.