March 2023 Market Summary

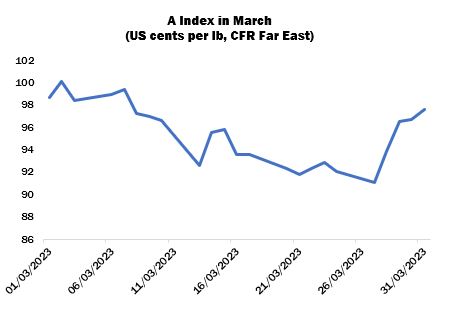

International cotton prices as measured by the Cotlook A Index moved lower to depart from their longstanding range in March, influenced by a collapse of New York futures mid-month, before reversing direction to end only modestly below their opening level. Uncertainty in the international banking system resulted in four consecutive days of decline for the lead May delivery, two of which recorded limit down settlements. However, prices staged a recovery in the subsequent sessions, as some confidence in the stability of the banking sector returned. The A Index registered its highest point for the period, of 100.10 US cents per lb, on March 2, while the value fell to a low of 91.05 on March 27, representing the weakest price since November 1.

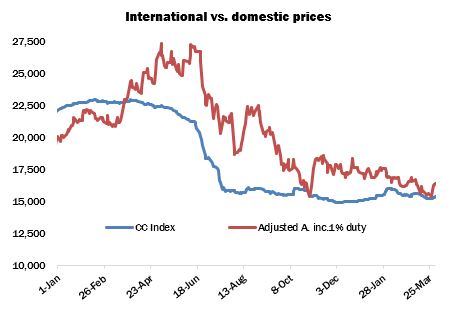

A flurry of import buying was witnessed as futures retreated below the 80-cent mark (allowing for landed prices well below one dollar). However, the volume of business concluded fell short of that which would normally be expected in the face of such an adjustment, and mills retreated to the sidelines as prices recovered ground. The major barrier to raw cotton purchases was the persistently weak state of demand in the cotton yarn market, and mill buyers in most countries lacked the confidence to make volume purchases beyond their nearby requirements.

Vietnam was one of the more active markets, with sales recorded for various origins including West African, Brazilian and US. Australian was also considered attractive, on quality and availability grounds. Meanwhile those countries which have for some time been experiencing issues associated with a lack of US currency reserves (most notably Pakistan and Bangladesh) continued to face difficulties in securing Letters of Credit and reports of new business were somewhat scarce during March. Mills with gaps in their nearby coverage bought modest volumes of various origins, including US and African Franc Zone styles, during dips in futures prices.

In China, the convergence of local and international values mid-month prompted some demand for imported lots. The bulk of enquiry was from state trading entities, but spinners also participated, albeit to a lesser degree.

US cotton captured the bulk of business during the downturn of the market, as reflected in reports of export sales registrations released during the month, predominantly on price considerations. The net increase in upland export sales registered during the first three weeks of March amounted to more than 800,000 running bales, of which China and Vietnam together account for nearly 65 percent. Shipments were also strong during the period, recording a seasonal high in the week ended March 23 and exceeding the average required to meet USDA’s latest forecast for the season (12 million bales of 480 lbs) on more than one occasion. However, the shifting of almost 90,000 bales destined to Pakistan into the 2024/25 marketing year reflected the protracted difficulties present in that country, and some observers anticipate further cancellations or deferments in the reports to come, should the financial situation fail to improve.

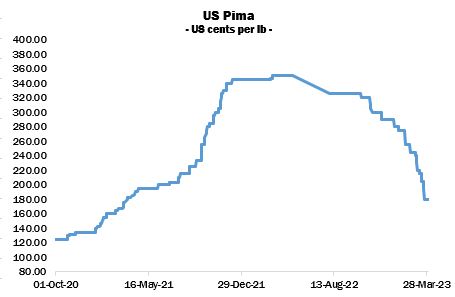

The reports also included two consecutive marketing year highs for Pima export registrations, following several months of very poor sales. Long staple prices have been under considerable pressure so far this season, with the result that in late March Cotlook’s US Pima price had been reduced by almost 45 percent since the beginning of August. Egyptian values have also undergone a steep downward adjustment, as some local sellers discounted their asking rates in an attempt to generate desperately needed US dollar income. Our first regular long staple market update appeared in the March 30 edition of Cotton Outlook, and will be available to subscribers on a monthly basis from now on.

Several major adjustments were made to our global production numbers for the current season during March, including increases for China and Australia that were partially offset by decreases for India and Brazil. In the first mentioned country, the near-ideal growing conditions in Xinjiang have resulted in a crop that has exceeded the threshold of six million tonnes for the first time, whereas in Australia, very wet conditions last autumn made for a difficult growing period for irrigated acres, but also facilitated the expansion of dryland plantings.

In India, a slight improvement in the pace of seed cotton arrivals was insufficient to dispel fears that the crop will fall well short of earlier expectations, and our number was lowered roughly in line with the latest number from the Cotton Association of India. Our Brazilian forecast was also trimmed, in accordance with a less optimistic view of yields. Expectations for the crop remained good, but the earlier confidence of the official forecasting agency that yields would reach record highs was tempered in its March report.

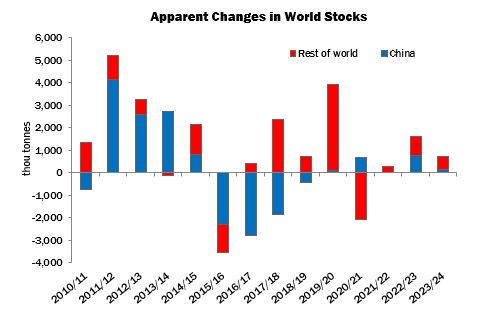

The result was a net increase to our assessment of world output of just 24,000 tonnes, to 24,916,000. Meanwhile, no changes were made to our assessment of global consumption in 2022/23, so stocks by the end of the current season are forecast to increase by 1,596,000, barely changed from a month earlier.

On March 31, USDA’s Prospective Plantings report indicated an area of 11,256,000 acres, modestly lower than the 11,419,000 projected by the National Cotton Council in April. Washington’s figure would mark a decrease of 18 percent from the previous season.

No significant changes were made to our figures for 2023/24: only a minor decline was recorded for production, which by the end of the month was placed at 25,394,000 tonnes (indicating a seasonal increase of slightly more than five percent), while consumption remained steady on the month. Ending stocks were therefore projected to rise by 841,000 tonnes, with the increase occurring predominantly outside China.