April 2024 Market Summary

New York futures again moved lower on balance during April. The July contract registered an even steeper monthly loss than that observed during March, at 1,045 cent points, to close at 81.52 cents per lb. The July/December spread narrowed further, to 160 cent points (July premium) by April 30, compared with 332 points at the end of the previous month and over 1,500 in late February. Turnover and open interest declined overall; particularly as speculative investors closed out their long positions in the expiring May contract. Certificated stocks meanwhile continued to rise.

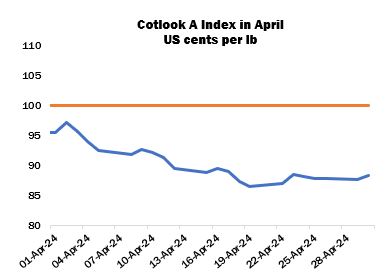

International offering rates, as measured by the Cotlook A Index, followed a similar trend to ICE, but fell by a smaller margin of 730 cent points over the month to end at 88.30 cents per lb.

The resultant increase in the premium of the A Index relative to ICE is explained by the recovery of basis levels offered by merchants, following their significant erosion (particularly for non-US growths) in March. Additional mill buying and fixations against on-call purchases were observed in a broad range of import markets, particularly for Brazilian and West African lots. However, the volatility of New York encouraged a cautious approach to fresh purchases, and weaker yarn prices in some markets likely discouraged spinners from extending their cotton coverage further. The realignment between local prices in India and international offering rates triggered some import demand from that market. Spinners’ buying interest was focused largely on African origins, many of which benefit from a partial reduction of import duty.

In China, Zhengzhou cotton futures ended the month lower too, closing at 15,700 yuan per tonne, down by 515 yuan from the end of April, a fraction of the decline in New York. Buyers in China were therefore active in the import market earlier in the month despite abundant local supplies as international cotton prices moved to a discount vis-à-vis the China Cotton Index, but the flurry of business slowed somewhat as the month progressed. Nonetheless, USDA export reports revealed that 252,500 running bales of net new sales were registered for China during the month in view, representing around half of the total for all destinations, while 389,300 bales were shipped to that destination. The Department increased its forecast of China’s cotton imports in 2023/24 from 12.9 million bales to 14.2 million in its April supply and demand estimates.

Meanwhile, planting of the 2024/25 crop expanded in Xinjiang to almost 90 percent complete by the end of April, although progress was delayed slightly in northern parts by persistent bad weather. Replanting, though, was not extensive and germination and early development were favourable.

In the United States, sowing expanded at about the same pace as recent averages. Beneficial rainfall was received in Texas, improving soil moisture and water reserves which may offer some very cautious optimism regarding the new crop’s prospects at this early stage.

Elsewhere, the government of Pakistan set a domestic production target for 2024/25 of 10.85 million local-sized bales, which would represent a significant increase from the output achieved during the season now ended. By the end of the month, around 20 percent of the target area (2.3 million hectares) had been sown, including 13 percent in Punjab and 38 percent in Sindh, and young plants progressed well under largely favourable conditions. In India, the first long-range forecast for this year’s Monsoon season was released, predicting above-average rainfall. The rainy season, including its timing and distribution, is decisive for cotton output in the country. Seed cotton arrivals from the current crop meanwhile continued to wind down, and the Cotton Corporation of India placed the total for the season by April 16 at 27.5 million lint equivalent bales.

Planting of shorter staple varieties began in southern growing regions of Egypt during the month in view. The area sown to cotton could increase by perhaps 25 percent according to some local observers. Sowing also progressed well in Greece, where area is expected to decline from that initially planted last year. Output, however, is hoped to be greater given that significant proportions were damaged by floods in 2023.

Meanwhile in the Southern Hemisphere, the outlook for Brazil’s crop remained largely positive. The official forecast put forward by CONAB was again increased, to 3.6 million tonnes, which would be a new record by some margin, while ABRAPA (the national cotton producers’ association) placed output at 3.5 million. Some market participants, though, anticipate an even higher figure. Rains in Argentina disrupted the early stages of picking, but the moisture was beneficial to plants still in the ground. Australia also experienced some harvest delays as a result of heavy rainfall, raising concerns that centred mainly on the grade composition of the crop.

Cotton Outlook’s forecast of world raw cotton output in 2023/24 was reduced by 8,000 tonnes in April, as an upward adjustment for Brazil was offset by declines for smaller producing countries. However, our estimate of production in 2024/25 was increased by 334,000 tonnes, attributed to Brazil, the United States and others. Our consumption figures were meanwhile left unchanged, therefore the margin by which production is expected to exceed consumption in the current season has narrowed slightly from the previous estimate to 593,000 tonnes. For 2024/25, global ending stocks are forecast to rise by 429,000 tonnes, up substantially from the 95,000 put forward last month.