May 2026 Market Summary

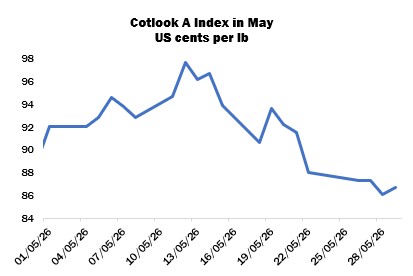

International cotton prices as measured by the Cotlook A Index experienced significant volatility in May, having reached a peak of 97.65 cents per lb on May 12 before falling back to end the month at 86.70 cents, down 1,095 from the peak and 235 points over the course of May. In New York, the July contract settled in a range of 1,162 points and lost 605 points on balance to close at 76.15 cents per lb. The July/December spread inverted to a July premium of 37 points on May 11 before widening to a 344-point new crop contract premium by the close of the last session in view.

In the first part of the month, import purchasing slowed significantly. Although yarn values had also made gains in recent weeks, they were unable to keep pace with raw cotton in many markets, and profit margins narrowed or turned negative. However, spinners with gaps in their requirements returned to the market as nearby futures retreated back below the 80-cent mark, although some anticipated further declines and opted to wait. The lower costs for raw materials allowed some enterprises to again achieve better margins on yarn sales, but downstream orders were also reported to have declined in some quarters.

Activity in Islamic markets slowed in observance of the Eid holiday at the end of May, although prior to the break business was arranged in Pakistan for various origins including US and Brazilian. Buyers in Bangladesh continued to issue enquiry for Brazilian and West African cotton, although price ideas were at times unworkable. Some forward sales were reported for early next year too. An uptick in purchasing was also noted in Turkey, while in Vietnam interest was observed for machine-picked cotton available afloat or for nearby shipment to meet immediate requirements. Selective demand emerged from China, and there were opportunities for sales at the China Cotton Industry Development Forum, but competitive basis levels were often needed in order to conclude business.

US export reports showed a net 456,500 running bales of upland were added to commitments for 2025/26 in the four weeks to May 21, while 1.22 million were shipped. Net sales registered for the next marketing year amounted to 406,100 bales. Total commitments for the season to that date advanced to 11.15 million bales, while accumulated exports were 8.6 million, still the lowest figures by that moment in a decade in both cases.

Planting beltwide was 53 percent complete by May 24, up slightly from last year but on par with the average. Work in Texas was three points behind the normal schedule, at 42 percent. Many key producing areas were still experiencing significant drought, so the arrival of fairly widespread precipitation late in the month was closely monitored by observers. While the rain was considered beneficial on balance, it was too early to say just how much impact it may have on yields and abandonment.

USDA’s May supply and demand report included the first detailed breakdown for 2026/27. Domestic production was projected at 13.3 million bales, down from the revised figure for the current season of 13.9 million. Exports were placed at 12.3 million (up from 12 million in 2025/26), and ending stocks were estimated at 3.9 million (versus 4.4 million).

As for the global balance sheet, output was pegged at 116.04 million (down from 122.64 in 2025/26). Consumption is forecast slightly higher on the year at 121.69 million, and ending stocks were lower at 71.84 million (77.27 million).

In China, prices on the Zhengzhou cotton futures platform rose strongly in the first session following the holiday at the start of the month. From there, though, the lead contract assumed a downward trend, eventually ending May at 16,110 yuan per tonne, a decline of 315 yuan from April 30, or a loss of 705 yuan (four percent) from the peak on May 6.

Meanwhile, the NDRC announced that the target price subsidy for Xinjiang cotton from 2026 to 2028 will be 18,600 yuan per tonne and based on a fixed output of 5.1 million tonnes, unchanged from the previous three years. Planting in the region was concluded with little interruption, but adverse weather in May affected young stands and slowed crop development in some parts.

The Indian government announced this month that the Minimum Support Prices for cotton in the 2026/27 season will be raised by around seven percent, a similar adjustment to previous years. Furthermore, an official project to increase yields in the country over the next five years was launched. The Mission for Cotton Productivity was granted a budget of approximately US$600 million to improve seed technology, planting systems and more.

This year’s Southwest Monsoon was expected to make landfall on May 26, ahead of the traditional start date of June 1, but had not yet reached the coast by the end of the month. Heavy pre-Monsoon rainfall was received in South India, while heatwave conditions persisted in the northwest of the country, where cotton planting usually begins in advance of the arrival of the Monsoon.

The long-range forecast published by the Meteorological Department in May for the weather system indicated a 10-percent reduction in total rainfall from the average.

Sowing approached a conclusion in key producing areas of Pakistan. Most stands were developing satisfactorily but some fields required replanting following high temperatures. Modest quantities of seed cotton began to arrive at gins, with work expected to pick up in June.

In the Southern Hemisphere, favourable conditions persisted overall in Brazil and local observers remained optimistic regarding yields. Picking began in pockets of the earliest sown areas. Grower sales of the 2026 crop amounted to 70 percent of the anticipated total by the end of May according to Abrapa. Good weather returned to Argentina’s cotton belt, allowing picking to expand. Harvesting approached a conclusion in Australia, where reports of yields and quality were positive. Here too, sales from first hands were encouraged by the rise in ICE futures earlier in the month.

Cotton Outlook’s forecast of global raw cotton production in 2026/27 was raised by 79,000 tonnes in May, to 25.45 million tonnes, as additions for the US and Turkey were only partially offset by a reduction for Pakistan. Our figure for consumption was meanwhile increased by 218,000 tonnes to 26.11 million, attributed to higher estimates for Bangladesh, Vietnam and India. The result would be a reduction of global stocks by the end of the next marketing year of 657,000 tonnes.

For the current campaign, global output is higher by 96,000 tonnes as larger figures for Brazil and smaller producing countries more than offset a decline for the African Franc Zone. Consumption was meanwhile raised by 332,000 tonnes. The estimated increase to global stock levels by August 31, 2026, has therefore narrowed to 342,000 tonnes.