May 2025 Market Summary

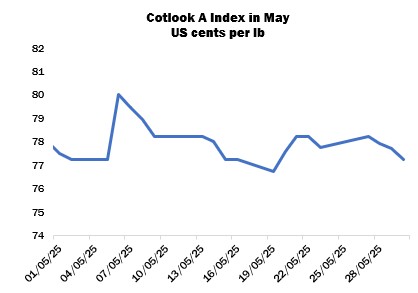

International cotton prices, as measured by the Cotlook A Index, strengthened early in May before moving lower again to end the month at 77.25 cents per lb, a fall of 75 points overall.

In New York, the July contract declined by the slightly greater margin of 96 points, to 65.06 cents per lb, its weakest close since early April (when Washington’s announcement of increased tariffs on many countries outside China caused pressure on prices).

The 275-point rally recorded for the July delivery on May 2 followed signals that Beijing was willing to engage in trade talks with the US. The respective governments met the following weekend in Geneva, and on May 12 a joint statement was released by the two parties, announcing that tariffs on imports of Chinese products to the US would be reduced to 30 percent, and those on trade in the other direction to ten percent, from May 14, for a period of 90 days. However, the reaction from the cotton futures market was muted. Later in the month, a US court ruled that the imposition of duties went beyond the scope of the emergency law used, but the administration immediately appealed and further hearings are due to take place in early June. In the meantime, the current levies remain in place.

Given the persistent uncertainty surrounding trade relationships for the coming months, mill buyers in most markets generally remained unwilling to commit to fresh business beyond nearby gap-filling. Nonetheless, merchants’ basis levels firmed slightly as futures declined, particularly since desirable supplies available nearby remained depleted or in strong hands at origin, and freight rates increased. Buyers in Southeast Asia, most notably Vietnam, though, secured some Australian lower grades as offers for such supplies increased owing to the untimely rain received during the growing period.

Interest from Bangladesh for Brazilian and West African persisted, but securing stocks at workable prices was often difficult. Spinners and garment manufacturers in that country also faced gas supply issues, which restricted operating rates for many enterprises. Meanwhile, India announced an immediate suspension of certain imports (including ready-made garments) from Bangladesh via the land border following Dhaka’s halt of yarn imports along the same route, thus raising concerns regarding the potential impacts on trade.

In China, the September delivery on the Zhengzhou cotton futures platform gained ground during the month in view, settling on May 30 at 13,270 yuan per tonne, up 495 yuan from the end of April. Plants in Xinjiang developed faster than in the past few years, and around one third of stands were in the squaring stage by the end of May. Yields were expected by some observers to increase further. Inspections of the 2024/25 crop in Xinjiang reached almost 6.68 million tonnes.

The US Department of Agriculture released its first detailed forecasts for the 2025/26 season on May 12. Domestic production was pegged at 14.5 million bales, above the estimate for 2024/25 of 14.41 million, and mill use at 1.7 million bales (unchanged). Exports were projected at 12.5 million (compared with the current season’s 11.1 million). Ending stocks are therefore placed at 5.2 million bales, versus 4.8 million in 2024/25.

World production is estimated at 117.81 million bales (121.07 million for the current season), domestic use at 118.08 million (versus 116.68 million), exports at 44.83 million (42.45 million) and ending stocks at 78.38 million (78.40 million).

Crop progress reports meanwhile indicated that US planting was around 52 percent complete by May 25, four points below the five-year average, while squaring was reported at three percent. Wet weather had delayed work in the Delta and Southeast, with flooding observed in some locales. Soil conditions in parts of West Texas had improved, but drought persisted in central and southern areas of the state.

Planting progressed well in Pakistan’s Punjab Province under hot weather, but a lack of water availability continued to hinder work in Sindh and some output estimates were revised downwards. Harvesting began on the earliest sown fields and a few ginning factories started operations.

In India, arrivals of 2024/25 crop cotton continued to slow, and the Cotton Corporation of India placed cumulative deliveries since October 1 at 27.7 million lint equivalent bales by the end of May. CCI auctions continued and around 400,000 bales were thought to have found buyers during the month, leaving 6.8 million in CCI hands.

A government press release published on May 29 confirmed that the Minimum Support Price for seed cotton will increase in 2025/26, by around eight percent for medium and long staple supplies. Meanwhile, the Southwest Monsoon made landfall over the coast of Kerala on May 24, a week before the traditional start date of June 1, and rapidly advanced over southern states. Rainfall during the season is expected to be six percent higher than the long-period average according to the Meteorological Department. Initial sowing began on irrigated fields in Haryana, Punjab, and Rajasthan, and perhaps 65-70 percent of the anticipated final total for the region was in the ground by the end of the month.

In the Southern Hemisphere, harvesting was under way in Brazil’s Bahia state, where stands have developed satisfactorily overall. In Mato Grosso, beneficial rains at a crucial moment meant that output expectations were revised upwards, although growers were monitoring pest infestations. In Australia, 80 percent of fields had been picked by the end of the month, and 20 percent of bales had been classed. Early results revealed a higher proportion of lower grades than is typical, due to untimely rains, but other quality parameters appeared favourable and greater clarity will be gained as work progresses. Wet weather meanwhile hindered picking in Argentina, where output estimates have been lowered in view of extended very hot, dry periods earlier in the growing season, followed by unwelcome precipitation over open cotton.

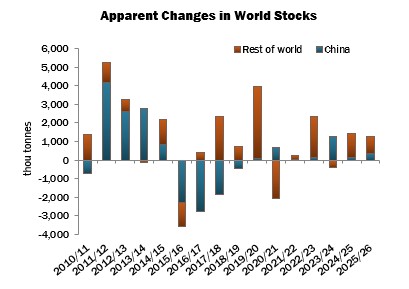

Cotton Outlook’s estimate of global raw cotton consumption in 2024/25 was reduced by 138,000 tonnes in May, to just under 24.6 million, as lower figures for India and Pakistan were only partially offset by increases elsewhere. World production was meanwhile subject to a modest revision, with the result that a larger addition to global stocks of 1,455,000 tonnes is estimated by the end of the season.

For 2025/26, our consumption forecast was also lowered, by 525,000 tonnes, to 24.42 million. Reductions were noted for China, Pakistan and India. Global output was raised by 371,000 tonnes, as increases for China, the United States, and others were partially offset by a decrease for Pakistan. Therefore, the margin by which production is forecast to exceed consumption in the next marketing year has increased to 1.25 million tonnes.