March 2026 Market Summary

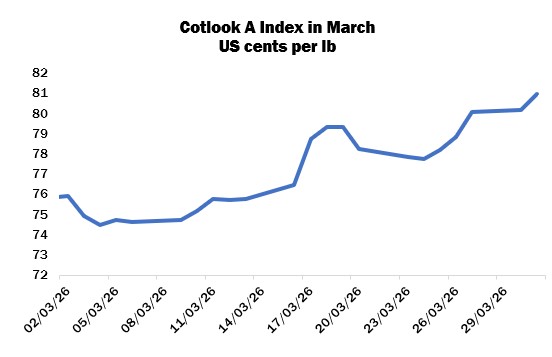

International cotton prices as measured by the Cotlook A Index rose strongly overall in March, ending the month at 80.95 cents per lb, a rise of 530 cent points from the end of February and its firmest level since early December 2024. In New York, the May contract gained 439 cent points to settle at 70.0 cents per lb.

Cotton futures, and wider markets, reacted to the outbreak of conflict in the Middle East and the subsequent effective closure of the Strait of Hormuz, a key shipping route for energy, fertiliser and other goods. The closure resulted in sharp increases to oil prices and to freight costs as many cargo ships were stuck or diverted via much longer routes.

Despite the uncertainty and higher prices (also reflected in stronger basis offers for many origins), import demand was relatively active, with the exception of a slight slowdown in Islamic markets during the Eid holiday. Many mills were in need of cotton to fulfil nearby requirements, particularly since yarn sales were also described as brisk in several markets and achievable returns had improved. That said, spinners and manufacturers expressed concerns regarding rising energy costs and limited supply following the disruption to shipping.

Mills in Vietnam were focused largely on US cotton, prompted by requests from retail buyers. In Bangladesh, spinners continued to secure Brazilian and West African lint, while those in Pakistan looked to secure recaps and other attractively priced cottons, although some mills without pressing needs paused procurement in view of the higher prices. Business was also described as active in Turkey, primarily for Brazilian and US supplies, as yarn demand and downstream orders picked up.

China was also mentioned, issuing demand for various origins, and the National Development and Reform Commission announced that 300,000 tonnes of Sliding-Scale import quota had been allocated to mills, to be applied against processing trade imports (for use in goods destined for export only).

A meeting between Presidents Xi and Trump was postponed owing to the war in the Middle East, but positive signals from talks provided some encouragement for those hoping for trade deals that may involve commitments to purchase cotton.

According to US export reports, the net addition to upland commitments for 2025/26 was 1.02 million bales in the four weeks to March 26, while 1.4 million were shipped. Vietnam remained the primary customer during the period, although sales to Turkey and China increased in the last week under review. Total commitments for the season so far amounted to 9.9 million bales, versus 10.4 million by the same date a year earlier. Accumulated exports were 6.06 million, compared to 6.38 million.

USDA published its Prospective Plantings report on March 31, providing a state-by-state breakdown of domestic area estimates for the upcoming campaign, based on surveys conducted earlier in the month. Total all-cotton area was placed at 9.64 million acres, up four percent from last year, including 9.51 million acres of upland (up four percent) and 130,000 of Pima (down eight percent).

Observers noted, however, that drought conditions were reported across much of the cotton belt, particularly in Texas, which may result in lower yields and higher abandonment if timely, widespread rains fail to arrive.

No changes were made to the US balance sheet for 2025/26 in the Department’s March supply and demand report, but global ending stocks were raised from 75.11 million statistical bales to 76.39 million, on account of a 1.1-million bale increase to production, and a slight decrease for consumption.

In China, the May contract on the Zhengzhou cotton futures platform ended the month unchanged at 15,330 yuan per tonne, having reached a peak of 15,570 in mid-March before falling back. Ginning in Xinjiang approached a conclusion, and inspections of lint in the region had reached over 7.5 million tonnes, up 12 percent on the year, while the volume inspected elsewhere was more than 100,000 tonnes. New crop planting commenced early in some parts owing to higher temperatures than usual during the month.

Elsewhere, robust sales were reported at the Cotton Corporation of India’s auction series, and prices were raised substantially, perhaps reflecting the sharp increase of values in the local open market, as well as the steady demand. The Cotton Association of India meanwhile raised its domestic production estimate for 2025/26 to 32.05 million local bales.

Sowing expanded in Pakistan under favourable weather. The Punjab provincial government offered incentives for cotton planting but growers there were less enthusiastic than those in Sindh due to the poor returns achieved last year. However, local prices increased strongly during the month, which may encourage some to proceed with cotton.

In the Southern Hemisphere, over 50 percent of stands were in the flowering stage in Brazil and perhaps 28 percent were forming bolls. Field reports were largely positive, although pest infestations were reported in Mato Grosso in late March. Sowing in Argentina was around 80 percent complete by the end of the month, while harvesting in Australia expanded.

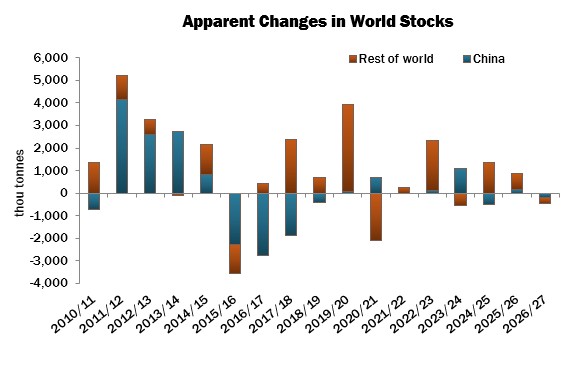

Cotton Outlook raised its estimate of global raw cotton output in the 2026/27 season modestly in March, as increases for Uzbekistan and smaller producers were almost offset by reductions for the US and China. Our figure for consumption was also increased, owing to higher numbers for China and India, among others. The result would be a reduction of global stocks by the end of the next marketing year of 295,000 tonnes.

For 2025/26, supply is higher by 194,000 tonnes on the month, again attributed to Uzbekistan and other producing countries, while our consumption estimate was raised by 254,000 tonnes in view of adjustments for several destinations.

The increase to global stock levels by August 31, 2026 is now projected at 1,000,000 tonnes, down from 1,060,000 in February.