December 2024 Market Summary

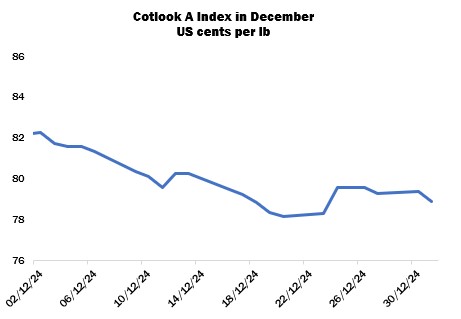

International cotton prices, as measured by the Cotlook A Index, fell by 310 points on the month, to be placed on December 31 at 78.90 cents per lb. That decline reflects a similar pattern in New York: the March contract ended December 353 points lower, at 68.40 cents per lb, hitting a life of contract low close on December 19 (67.91 cents per lb), before rebounding somewhat. Only four positive settlements were recorded during the month. Daily volumes were lighter than in the previous period, particularly in the latter half of December as a holiday mood prevailed.

Despite the holiday considerations in many markets, regular import demand was reported, likely encouraged by lower prices as well as an ongoing need for some mills to cover against nearby gaps in requirements. In that vein, buyers in Bangladesh secured Brazilian and West African supplies, predominantly for nearby shipment. Lower grade lots from various origins found buyers in Pakistan as the availability of local cotton declined and prices began to firm. Mills in Vietnam were price sensitive but routine business was confirmed over the month. Turkey, on the other hand, was active in procuring supplies from the international market as local values remained unworkable for many buyers. Brazilian and US supplies were in focus, and US export reports in December confirmed robust registrations to Turkey: in the four publications covering the period up to December 26, Turkey increased its commitment for the current season by 191,400 running bales, accounting for 25 percent of the total new registrations in that time frame.

Meanwhile in China, the January and May contracts on the Zhengzhou cotton futures platform also declined during the month, each losing 550 yuan per tonne. The former delivery recorded a life of contract low settlement on December 19, at 13,315 yuan.

Ginning in Xinjiang reached almost six million tonnes by the end of December, around 92 percent of Beijing Cotton Outlook’s revised forecast of total output for the region (6,492,000 tonnes). The China Cotton Association increased its estimate of total production, to 6.44 million tonnes, while Cotton Outlook’s figure was revised upwards to 6.8 million. Demand, however, remained pedestrian and many mills reported that they planned to suspend their operations for an extended period around the Lunar New Year holiday in view of slow yarn sales and rising financial pressures.

In the United States, the Department of Agriculture made a modest adjustment to its domestic balance sheet: a 64,000-bale increase to 2024/25 production brought the figure to 14.26 million 480-lb bales. The Department’s forecast for world output was also raised, from the 116.18 million bales put forward in November to 117.39 million, attributed to a large increase for India, and higher figures for Argentina, Benin and Brazil. Consumption was raised by 570,000 bales, to 115.79 million, resulting in a slight increase to ending stocks, to 76.02 million bales.

US growers meanwhile began to assess planting options for the upcoming season, with many analysts expecting a smaller planted area in view of higher costs and lower futures prices.

Seed cotton arrivals continued to slow in Pakistan: according to the Cotton Ginners’ Association, deliveries totalled almost 5.5 million lint equivalent bales by December 31, up by 261,500 bales from the end of November. Following several weeks of stagnation, local prices firmed late in the month as available stocks, particularly better grades, were in tight hands and mills became increasingly willing to pay more to cover their requirements. In India, arrivals remained robust at over 200,000 bales per day. The Cotton Corporation of India had bought 3.5 million bales by the end of December, mostly from Telangana, exceeding the almost 3.3 million procured in total last season. Sales of 2023/24 crop supplies amounted to just over 2.6 million bales, while the auctioning of lots from the current season were yet to begin.

Seed cotton auctions recommenced in Egypt on December 15, with the opening prices representing a discount of E£2,000 from the minimum guaranteed prices announced in February. More than 70 percent of the total output had been sold from first hands by the end of the period in view. According to Alcotexa, export registrations had reached almost 12,000 tonnes by December 28, still below the 20,000 registered by the same point last year. Giza prices in the export market came under pressure owing to the now assured availability of Egyptian cotton and the lower prices paid by merchants to growers.

In Brazil, ginning of the 2024 crop drew to a close, while early sowing of the new crop had begun in some parts. The official forecasting agency CONAB reduced its 2024/25 output figure slightly to 3,694,000 tonnes, and ABRAPA, the producers’ association, lowered its own projection to 3.91 million tonnes. The exporters’ association, ANEA, meanwhile increased its figure to 3.88 million.

Planting in Argentina was essentially complete by the end of the month, and rainfall was received in several locales, to the benefit of young stands. Area estimates still varied widely, ranging between 650,000 and 800,000 hectares. The Australian Cotton Shippers’ Association meanwhile noted that ginning and classing of the 2024 crop was complete. New crop sowing in that country was well advanced, and the World Meteorological Organization forecast that helpful rainfall could be brought by La Niña conditions in the coming months.

In December, Cotton Outlook’s forecast of world raw cotton production in 2024/25 was raised by a further 449,000 tonnes, to 25.98 million, to reflect a large increase for China as well as smaller, but still substantial additions for India, Argentina and the United States. Our consumption estimate was meanwhile reduced by 65,000 tonnes to 24.44 million, as a lower figure for China more than offset an increase for Pakistan. As a result, world stocks at the end of the current season were expected to rise by 1,534,000 tonnes, compared to the 1,020,000-tonne increase indicated a month earlier.

Adjustments to Southern Hemisphere output in 2023/24 mean that the margin by which production is estimated to have exceeded consumption in that campaign increased slightly, to 917,000 tonnes.