April 2025 Market Summary

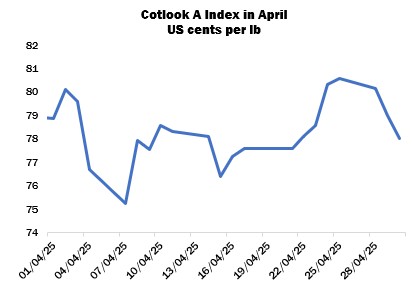

The Cotlook A Index, representing international cotton prices, was notably volatile during April, but ended the month only modestly lower overall at 78.00 cents per lb (down 90 points). In New York, the July contract settled within a range of almost four cents, but declined by 197 cent points overall to close at 66.02 cents per lb.

Much of the volatility during the period under review was attributed to trade policy developments in the US. On April 2, Washington announced a swathe of new import tariffs on goods from almost every country in the world. The rates applied ranged between 10 and 49 percent, including 46 percent on products from Vietnam, 37 on those from Bangladesh, 30 for Pakistan and 27 for India – key textile manufacturing and exporting markets. For China, a 34-percent duty was set in addition to the 20 percent already in place, bringing the total to 54. The July ICE futures contract lost 462 cent points in the three sessions following the announcement and posted record daily volumes, while financial markets also tumbled dramatically.

As markets attempted to grasp the potential impacts of the tariffs on trade, economic growth, and inflation, for example, Washington then announced on April 9 that a 90-day pause would be implemented on the duties (other than the baseline 10-percent levy) to allow time for negotiations with various countries, with the exception of China. Beijing had responded to the 34-percent levy on its goods arriving in the US with a duty on US imports of the same magnitude, which was followed by a series of retaliatory increases culminating in 125 percent on Chinese goods entering the US and 145 percent on products and raw materials travelling in the other direction. Later in the month, the US administration suggested talks were taking place with China, but Beijing denied that communications had begun, dampening hopes of a swift resolution.

In the physical market, mill buyers tended to approach new business with caution in view of the tariff announcements and the prospect of severely disrupted patterns of trade. Piecemeal, hand-to-mouth sales were reported for those spinners with gaps to fill, such as in Bangladesh, but elsewhere many markets were quiet. In some quarters, it was suggested that increasing imports of US cotton could be used as a part of wider efforts to reduce trade deficits with that country and aid negotiations, although some buyers noted that such a strategy might be impractiable on price grounds unless government support could be given to offset costs.

In China, meanwhile, the May delivery on the Zhengzhou cotton futures platform lost almost eight percent of its value during April, to close at 12,490 yuan per tonne (down 1,055 yuan). Planting was complete in Xinjiang by the end of the month, and seedling emergence was evident on two thirds of fields. Some replanting was necessary in northern and eastern parts of the region, though, due to high winds in early April. Inspections of the 2024/25 crop in Xinjiang reached 6.67 million tonnes.

In its latest supply and demand report, USDA left its domestic 2024/25 figures unchanged except for a reduction of 100,000 480-lb bales for exports, to 10.9 million, resulting in an increase in ending stocks by the same margin to 5.0 million bales. Its global estimates were again adjusted slightly, including higher production and beginning stocks and lower consumption and trade, with the result that world ending stocks edged up to 78.86 million bales.

US crop progress reports indicated that 15 percent of cotton fields had been planted beltwide by April 27, one percentage point ahead of last year’s corresponding figure and the five-year average. Progress was most advanced in California, where 50 percent of fields had been sown, while work in Texas had reached 21 percent complete. During the month in view, helpful rains were received in Texas and the Southeast where drought conditions had been prevalent in many parts, although additional precipitation would be welcomed in many fields.

Elsewhere in the Northern Hemisphere, planting accelerated in Pakistan, and a modest improvement in water availability was noted in Sindh, largely as a result of snowmelt as temperatures increased. Progress was still behind last year’s pace, but was slightly more advanced in Punjab. Water concerns were compounded, however, by India’s suspension of the Indus Waters Treaty following an attack in Kashmir. A retreat from the key water sharing agreement raises concerns that river flows could be disrupted with severe impacts on agricultural land already increasingly facing floods and droughts in recent years. Protests also erupted in Pakistan against proposals to build new canals on the Indus River, blocking highways and thus disrupting the transportation of goods in Punjab and Sindh.

Meanwhile, the Indian Meteorological Association released its first long range Monsoon forecast for the season, indicating that rainfall is likely to be above average. The Cotton Corporation of India placed cumulative arrivals since October 1 at 27.3 million lint equivalent bales by the end of April, up from 26 million by late March. CCI auctions continued and 950,000 bales were thought to have found buyers during the month, leaving 7.2 million in CCI hands.

In the Southern Hemisphere, stands in Brazil generally progressed satisfactorily, although persistent rains in parts of Bahia resulted in some losses of lower bolls. In Australia, clear weather allowed picking to expand later in the month, and ginning had begun in some regions. March’s untimely precipitation is thought to have affected the grade composition of the crop, but estimates of output were placed at around 5.0-5.2 million local bales. Grower sales accelerated as the Australian dollar depreciated versus the US currency, making selling prices more attractive for a period. Intermittent showers disrupted picking in parts of Argentina. Progress had reached around 30 percent complete in Chaco Province by the end of the month, and 24 percent in Santiago del Estero.

Cotton Outlook’s estimate of global raw cotton production in 2024/25 was reduced to 26.06 million tonnes in March, as an addition for Turkey was more than offset by lower figures for the African Franc Zone and smaller producing countries. Our consumption figure was meanwhile decreased by 118,000 tonnes, attributed mostly to downward adjustments for China, Bangladesh and Vietnam. Therefore, the margin by which production is estimated to exceed consumption in the current season has increased to 1.32 million tonnes

For 2025/26, various adjustments were made to our output forecasts resulting in a marginal overall rise, while forecast consumption was increased by 12,000 tonnes. The result would be a slightly smaller addition to world stocks by the end of the next marketing year, of 356,000 tonnes.