August 2024 Market Summary

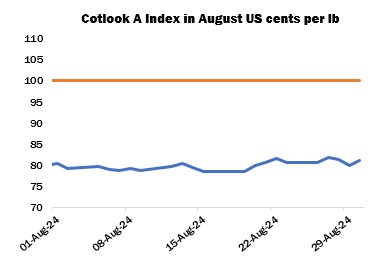

International cotton prices, as measured by the Cotlook A Index, increased slightly overall during August to end the month at 81.20 cents per lb – a rise of 135 cent points from the end of July. Fluctuations were relatively narrow, following the trend observed in New York futures.

Market observers digested a range of factors as the month progressed. In the United States, crop health improved moderately across the cotton belt. The proportion rated ‘poor’ to ‘very poor’ declined from 27 to 24, while 32 percent was considered ‘fair’ (up from 28) and 44 rated ‘good’ or ‘excellent’, about unchanged. Blooming and boll opening were ahead of the normal pace by September 1, at 94 and 37 percent respectively.

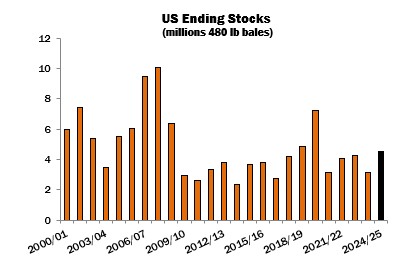

However, in its August supply and demand forecast the Department of Agriculture reduced its 2024/25 domestic output figure by 1.9 million bales (480 lbs) to 15.1 million bales, on account of lower acreage and higher abandonment estimates. US beginning stocks were adjusted upward slightly and exports were reduced, all of which resulted in a forecast ending stock of 4.5 million bales, below the 5.3 million put forward in July, but which would nonetheless be the highest since 2019/20.

China’s Zhengzhou cotton futures platform meanwhile declined further during August, the September contract conceding 540 yuan per tonne in total. That delivery posted a new life-of-contract low settlement on August 19 at 13,245 yuan per tonne, before closing the month at 13,555 yuan. Chinese import demand was subdued, as domestic supplies were abundant and yield estimates for 2024/25 continued to grow. Physical prices for local cotton also declined, reducing the incentive to import. The 200,000-tonne quota announced at the end of July was not immediately released to mills, although the additional allowance may already have been accounted for in existing commitments or earmarked for consigned stocks, which were also substantial.

Mill buying in most other markets continued in a largely hand-to-mouth and price-sensitive fashion during August, picking up slightly when futures dipped. However, the prospect of smaller local crops in India and Pakistan this season, as well as relatively strong prices for limited domestic supplies, encouraged import buying from that quarter. The origins in focus included Brazil, West Africa, the US and Australia.

The area sown to cotton has fallen short of expectations in both India and Pakistan (although planting is not yet complete in the former country, the figure by the end of August was almost ten percent behind the same point last year), and torrential rains and flooding towards the end of the month created additional concerns regarding the health of the standing crop. In India, market estimates of the impact of the floods varied widely and official assessments were awaited.

Local observers in Pakistan also monitored the effects of persistent wet weather. Growers reported waterlogging in some fields and assessed the possibility of pest infestations. Official arrivals data indicated that deliveries were 60 percent behind last year by August 31, and early forecasts of the final output have been scaled back.

Meanwhile, civil unrest continued in Bangladesh early in the month, culminating in the resignation of Prime Minister Sheikh Hasina on August 5 and the establishment of an interim government. Spinners and garment manufacturers reopened and worked to catch up on delays resulting from the disruption, although banking services such as document processing had fallen behind and backlogs at ports also had to be cleared to allow imports and exports to resume.

However, flooding in the latter part of the month also affected Bangladesh, particularly eastern areas, resulting in obstructed routes to and from Chattogram Port, again creating additional delays. While it was reported that most garment buyers did not cancel orders following the unrest and disruption, tight lead times remain difficult to meet, and manufacturers hope that a level of stability will be maintained in the coming months to allow normal operations to continue and to avoid the diversion of orders to other countries.

Nonetheless, some import buying continued during August where possible, often for West African or Brazilian lots to cover nearby requirements. Those with urgent gaps to fill paid premiums for supplies available afloat.

In the Southern Hemisphere, the Brazilian harvest approached a conclusion. IMEA estimated Mato Grosso’s progress at 87 percent by the end of August, while work in Bahia was also nearing completion. Very good yield and quality results were maintained. Meanwhile, clear skies aided the progress of final picking in Argentina, while early planted seedlings began to emerge in Australia. In that country, 2024/25 output was estimated at one million tonnes by ABARES, up from its previous forecast but representing a decline of seven percent from its figure for 2023/24.

Cotton Outlook’s forecast of world raw cotton output in 2024/25 was lowered by 332,000 tonnes in August, reflecting reductions to our figures for the United States, Pakistan and the African Franc Zone, only partially offset by higher figures for China, Turkey and Greece. Our estimate for 2023/24 was also reduced slightly, owing to a downward adjustment for Pakistan. Our global consumption figure was decreased by 310,000 tonnes for the current season but was increased by 107,000 for 2023/24. Therefore, the margin by which output is estimated to have exceeded consumption in the now concluded 2023/24 season has narrowed to 951,000 tonnes, whilst the projected surplus for 2024/25 has declined slightly to 745,000.