April 2026 Market Summary

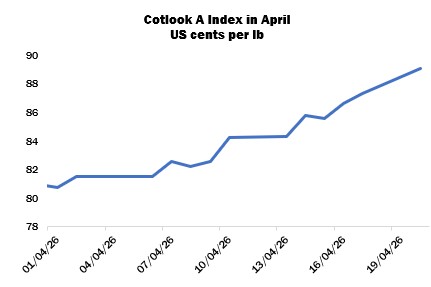

International cotton prices as measured by the Cotlook A Index rose sharply further in April, ending the month at 89.05 cents per lb, an increase of 810 cent points from the end of March. A high of 90.55 cents was achieved on April 22, its firmest level in two years. In New York, the July contract strengthened by just over 10 cents overall, to settle at 82.2 cents per lb, recording a limit-up move in the last session under review.

Oil prices and freight costs remained high as traffic through the Strait of Hormuz continued to be restricted and a resolution to the conflict in the region failed to be reached despite negotiation attempts and ceasefire announcements.

Spinners took a more cautious approach to new business in April in view of the uncertainty and price volatility. Many reported active yarn sales and good margins as they worked through cotton supplies purchased earlier at lower levels. However, few had covered their requirements for the months ahead and would therefore need to return to the market soon enough. Profits could thus be squeezed as yarn values failed to keep up with the increases for raw materials in many cases.

Mills in Pakistan often had to turn to the international market as domestic supplies dwindled and prices rose sharply. Those in Bangladesh continued to procure West African lint as well as Brazilian, including some new crop cotton, although many enterprises reported low operating rates due to energy shortages. Buyers in Vietnam were apprehensive in committing to volume purchases, but US cotton remained in focus for those with gaps to fill. Activity in Turkey slowed from the more brisk pace reported last month, but some additional Brazilian and US sales were noted as well as Greek due to the much quicker transit times.

US export reports indicated that the net addition to upland commitments for 2025/26 was 763,500 running bales in the four weeks to April 23, while 1.3 million were shipped. Net sales registered for the next marketing year totalled almost 204,000 bales. Total commitments for the season to that date amounted to 10.7 million bales, while accumulated exports were 7.4 million, the lowest figures by that juncture in a decade in both cases.

Sowing expanded across the US cotton belt, reaching 16 percent of the anticipated total by April 26 (versus a five-year average of 13 percent), up two percentage points from the same moment last year. Work in Texas was 20 percent complete, on a par with 2025. Observers monitored weather forecasts and the possibility of rain closely, as many key producing areas remained in drought as the growing season commenced. Some precipitation was received towards the end of the month, but more would be needed to alleviate dry soils.

In its April supply and demand report, USDA again made no changes to the domestic balance sheet for 2025/26. However, amendments to the global figures included higher beginning stocks, production, and consumption, but slightly lower trade, with the result that ending stocks were raised from the 76.39 million bales estimated in March to 77.04 million.

In China, prices on the Zhengzhou cotton futures platform gained strong ground. The lead September contract rose by 965 yuan per tonne to close the month at 16,425 yuan. The China Cotton Association issued a warning to the local industry regarding the volatility, and some observers contemplated the possibility of interventions such as State Reserve auctions. Meanwhile, new crop cotton sowing approached a conclusion in Xinjiang and seedlings were rapidly emerging.

Planting continued to advance in Pakistan under mostly open skies. Some growers were encouraged to proceed with cotton over alternative crops and invest in inputs due to the high local prices achievable. However, those in Punjab were more reluctant owing to disappointing yields and poor returns in previous seasons.

Domestic prices also continued to advance sharply in India. Relatively active sales were noted at the Cotton Corporation of India’s auction series, amounting to almost 100,000 local bales (versus perhaps 170,000 bales in the previous month), and floor prices were raised markedly.

In the Southern Hemisphere, field reports from Brazil remained largely positive, and some estimates of final production were increased. Grower sales of the 2026 crop accelerated, and exports were also strong. Picking advanced in Australia under clear weather, but work in Argentina was interrupted by wet conditions with progress in Santa Fe placed at just 15 percent by the end of the month.

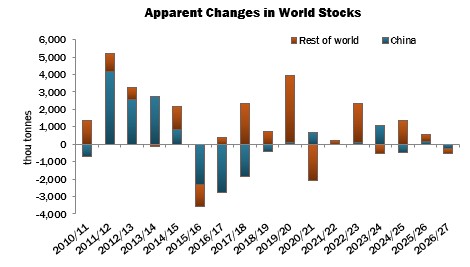

Cotton Outlook’s forecast of global raw cotton output in 2026/27 was increased by 264,000 tonnes in April, to 25.37 million, attributed almost entirely to additions for China and Pakistan. Our figure for consumption was meanwhile raised by 487,000 tonnes to 25.89 million, owing mainly to higher estimates for China, Pakistan and Turkey. The result would be a reduction of global stocks by the end of the next marketing year of 518,000 tonnes.

For the current campaign, world supply is higher by 110,000 tonnes as larger figures for India and Brazil were only partially offset by declines for smaller producing countries. Consumption was raised by 532,000 tonnes on account of various adjustments. The increase to global stock levels by August 31, 2026, therefore narrowed from one million tonnes estimated in March, to 578,000.