June 2026 Market Summary

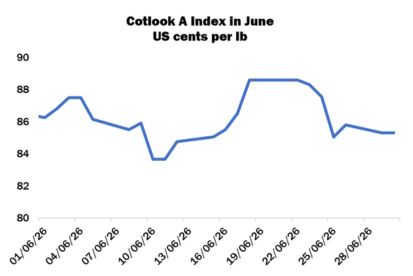

International cotton prices as measured by the Cotlook A Index moved in a range of just under five cents per lb in June, declining by 140 points overall to end the month at 85.30 cents per lb. In New York, the December contract lost 279 points on balance, having reached a high of 80.54 cents per lb on June 2, and a low of 75.30 cents a week later. The July delivery had its First Notice Day on June 24. Total Open Interest fell by 32,579 contracts from the end of May, to 305,708, and daily volumes had declined by the end of the period.

In the physical market, import purchasing was of routine proportions throughout most of the month. Pakistan had been active in May, but most buyers turned away from international business as local new crop arrivals picked up and prices declined. In Bangladesh, Brazilian and West African supplies remained in focus, but mills were particularly price sensitive as they continued to report high energy costs and squeezed margins. Moderate sales were noted in Turkey to fulfil nearby requirements, but downstream demand slowed as the quieter summer period began. In Far Eastern markets, activity was rather subdued, with modest quantities booked by those with gaps to fill but price ideas were often unworkable. Demand from China was also slow, hampered in part by limited import quota and relatively weak yarn business. The quantity of consigned stocks at ports was also sizeable.

Meanwhile, the Indian government announced the suspension of the customs duty on cotton imports from June 1 through to October 31. Only tentative interest in international supplies was noted at first, but enquiry picked up later in the month while purchases from the Cotton Corporation of India were also robust.

US export reports showed a net 517,000 running bales of upland were added to commitments for 2025/26 in the four weeks to June 25, while 1.07 million were shipped. Net sales registered for the next marketing year amounted to 598,000 bales. Total commitments for the season to that date advanced to 11.85 million bales, while accumulated exports were 9.95 million.

USDA released its Planted Acreage report on June 30, placing all-cotton beltwide area at 9.85 million acres, versus the 9.64 million published in the March Prospective Plantings report, and six percent greater than last year’s eventual figure of 9.28 million. Sowing was virtually complete by the end of the month, in line with the five-year average.

In its June supply and demand publication, the Department left its US production estimate unchanged at 13.3 million bales. Some observers had expected an increase due to the fairly widespread rains received over the past month or so that had alleviated drought conditions in many growing regions, although it was noted that other fields had become inundated.

As for the global balance sheet, output was also maintained, at 116.04 million bales. Consumption was raised to 121.76 million (121.69 million in the previous report), while exports were lowered slightly to 43.32 million. Ending stocks were placed at 71.13 million, versus the 71.84 million projected in May.

In China, the lead September contract on the Zhengzhou cotton futures platform settled in a range of 690 yuan in June, to end the month just 30 yuan lower overall at 16,080 yuan per tonne. Around half of cotton stands in Xinjiang were blossoming by late June, but high temperatures and water shortages resulted in some boll shedding and increased pest counts.

The Southwest Monsoon made landfall on June 4, slightly later than the traditional start date of June 1. By the end of the month, the system had advanced to cover Maharashtra and parts of Gujarat and Madhya Pradesh, but overall rainfall was 40 percent below the Long Period Average, with the biggest deficiencies in key central cotton areas.

By June 25, almost three million hectares had been sown to cotton across the country, 35 percent below the figure reported at the same moment a year earlier. Work was significantly behind in the important growing states of Maharashtra and Gujarat.

In Pakistan, stands were generally developing well although some required additional precipitation following prolonged periods of hot and dry conditions. Early arrivals picked up to around 15,000-20,000 local bales per day, and more gins began work for the season.

In the Southern Hemisphere, picking began in Brazil with around four percent of the crop gathered by late June. Inclement weather in Mato Grosso and Bahia delayed field work slightly but local observers remained optimistic regarding final output. Harvesting progressed in Argentina but was periodically disrupted by wet conditions. Production forecasts were revised downward in some cases. Picking was essentially complete in Australia and quality reports were positive.

Cotton Outlook’s forecast of world raw cotton output in 2026/27 was raised by a further 185,000 tonnes in the month, to 25.64 million tonnes, as a higher figure for the United States was only partially offset by a reduction for Pakistan. Our consumption figure was meanwhile increased modestly to 26.16 million tonnes. The result would be a reduction of global stocks by the end of the next marketing year of 517,000 tonnes.

For the current campaign, our global production figure has been maintained at 26.56 million tonnes, while consumption was raised by 271,000 tonnes to 26.49 million owing to adjustments for several major markets. The estimated addition to global stock levels by August 31, 2026, has therefore narrowed further, to 71,000 tonnes.