October 2025 Market Summary

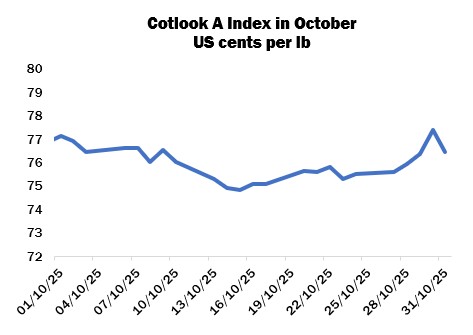

International cotton prices, as measured by the Cotlook A Index, declined by just 45 cent points overall in October, ending the period at 76.45 cents per lb. The Index fluctuated within a range of 255 points, having reached its lowest level in five years on October 15 before regaining ground. The December delivery in New York, meanwhile, ended the month only 23 points lower on balance, reaching a new contract low close of 63.51 on October 14 before assuming a more positive trend. Open interest rose further, reaching 298,906 contracts on the last day of the month, its highest level since 2018.

The US Federal Government shut down on October 1 after Congress failed to agree on a spending package, marking the first government shutdown since 2018. Most reports issued from USDA were suspended as a result, and growers had no access to Marketing Loan payments. Indications that Farm Service Agency (FSA) operations were to resume circulated late in the month, but progress in that regard appeared to be slow and growers remained without financial support. Cotlook’s calculations of the Adjusted World Price that would have applied in the two weeks between October 17 and 30 had fallen below the loan level of 52 cents for the first time since March.

Meanwhile, President Trump threatened 100-percent tariffs on China in reaction to Beijing’s announcement of tighter controls on rare earth exports, which was followed by the addition of port charges for ships registered in the opposing countries. Despite the escalating hostilities, reports circulated that Xi and Trump were still set to meet in South Korea during the Asia-Pacific Economic Cooperation Summit in late October. Bullish trends were observed across many markets, including cotton futures, in the run up to the meeting as observers anticipated a trade deal, but the outcome failed to live up to most expectations. In the event, duties on Chinese products entering the US were reduced by ten percent, but remained high at perhaps an average of 47 percent, while Beijing was said to have agreed to restart purchases of US soybeans after a longstanding pause. Comments from the US President implied that other farm products may also be included in arrangements, but cotton was not mentioned specifically.

The 2025 ICA Trade Event held in Dubai earlier in the month provided an opportunity for some raw cotton business, and reports emanating from the conference and in the days and weeks following noted moderate sales, mostly for Brazilian cotton. Mills with gaps in their coverage looked to secure supplies at advantageous prices, although yarn values also declined in most markets, squeezing spinners’ profit margins, and few were willing to depart from their longstanding hand-to-mouth purchasing style.

Sales to India slowed as the window for duty-free shipments narrowed, while auctions held by the Cotton Corporation of India continued to offer susbtantial volumes. In Pakistan, some import business was noted as international prices fell, but in general buyers were focused on procuring domestic supplies as arrivals peaked. Mills in Bangladesh looked to take advantage of price dips, securing mostly Brazilian and West African cotton, but continued to face difficult operating conditions and issues accessing finance and Letters of Credit.

Many spinners in Vietnam were thought to have covered their requirements until the end of the year, so activity in that market was relatively subdued. In Turkey, harvesting of the domestic crop picked up but prices were still higher than many buyers were willing to contemplate. As a result, some import business was concluded, largely for Brazilian lint, but the overall mood in the spinning sector remained downbeat as high costs and weak demand persisted.

Following the return from the National Day and Mid-Autumn Festival holidays in China at the beginning of the month, prices on the Zhengzhou cotton futures platform reopened on a positive note before falling back somewhat. An upward trend then resumed, and the January contract ended the month 390 yuan higher overall, closing at 13,635 yuan per tonne.

Picking approached a conclusion in Xinjiang, and almost 1.92 million tonnes of lint had been inspected by October 31 from a total of 968 ginners in the region, according to data from the China National Cotton Exchange.

The last crop progress report published by USDA before the government shutdown, covering the week ended September 28, indicated that beltwide boll openings were at 67 percent, and the proportion of stands harvested was placed at 16 percent. By the same date, 47 percent of plants were judged to be in good or excellent condition, while 36 percent were considered fair, and 17 percent were poor to very poor. In absence of USDA reports, observers attempted to consider how crop prospects might have changed since the last output forecast of 13.2 million bales, as well as the pace of exports from that country.

Pakistan arrivals reached a peak in October before slowing somewhat. According to PCGA, arrivals by the end of the month totalled over 4.4 million lint equivalent bales, an increase of almost 1.4 million bales from September 30, representing a rise of three percent from the comparable figure a year earlier. Some observers raised their estimate of final output slightly as field work progressed.

In India, new crop arrivals gradually picked up pace, although a dip was observed during the Diwali holiday. Daily estimates later in the month, though, were behind those during the same timeframe of the previous two seasons, and a powerful cyclone brought heavy rains and strong winds to southern states in late October, threatening cotton fields. Cotton Corporation of India procurement operations for the 2025/26 crop began, while sales of 2024/25 supplies continued.

Picking in Greece approached a conclusion, and output estimates circulated in a wide range. Seasonal rainfall was welcomed as beneficial for soil moisture and water storage replenishment. Harvesting progressed in Turkey, with work reaching 20-25 percent complete in the Aegean region, and between 30 and 50 percent in the east of the country. However, untimely rains in the Aegean area were said to have affected yields and quality.

In the Southern Hemisphere, observers indicated that the area dedicated to cotton in Brazil may decline in the upcoming campaign, as growers are dissatisfied with increasing costs and low prices, although recent forecasts by various organisations offer slightly differing views. Meanwhile, planting proceeded across parts of the Australian cotton belt, with seedling emergence reported in some areas. Ginning of the 2025 crop approached a conclusion. Welcome rainfall was received in Argentina’s cotton fields, which should benefit the expansion of new crop sowing.

Cotton Outlook’s forecast of global raw cotton production in 2025/26 was reduced by 147,000 tonnes in October, as lower figures for Brazil, the United States and other countries were only partially offset by increases for Pakistan and the African Franc Zone. A moderate upward adjustment to our 2024/25 estimate was attributed largely to Brazil.

Our consumption forecast for the current campaign was raised by 38,000 tonnes, mostly as a result of increases for Pakistan and Vietnam, while a modest reduction was made to our 2024/25 figure.

Therefore, the margin by which output is estimated to have exceeded consumption last season widened to 820,000 tonnes, whilst the projected surplus for 2025/26 declined to 338,000.