November 2025 Market Summary

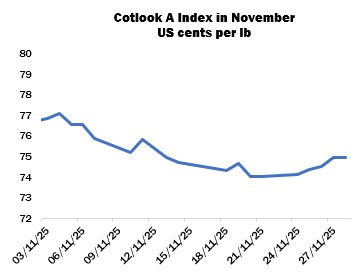

International cotton prices as measured by the Cotlook A Index followed a largely downward trajectory last month, reaching a low point of 74.00 cents per lb on November 20, a level not seen since October 2020, and losing 150 cent points overall. In New York, the December delivery made new contract low closes as it approached its expiry, as did the now lead March contract (of 63.74 cents per lb), although a modest recovery then followed. Record daily volumes were traded earlier in the month as positions were rolled from December to March, while open interest remained robust, peaking at 311,545 contracts on November 6.

A resolution to the US government shutdown was reached on November 12, after 43 days of limited federal operations, the longest shutdown in history. USDA functions subsequently resumed. On November 13, the first export report (covering the week ended September 25) was released, following which two reports a week were planned until the normal schedule is resumed. In the period between September 25 and October 16, it was revealed that upland exports totalled 687,713 running bales, while shipments were 574,203 bales, bringing accumulated exports to 1,495,317 bales.

On November 14, USDA released an updated supply and demand report, the first since September 12. For the domestic balance sheet, production was increased to 14.1 million bales, up from 13.2 million in the last publication, while exports were raised by 200,000 bales to 12.2 million, leaving the estimate for ending stocks at 4.3 million (3.6 million in September). However, many observers met the addition to the export projection with some uncertainty, in view of the pace of sales reported thus far, while the 900,000-bale increase to output was greater than some had anticipated.

For the global balance sheet, production in China and Brazil were also raised, and the estimate of total consumption was slightly higher, while adjustments to trade and beginning stocks all resulted in a rise of 2.8 million bales for world ending stocks, to 75.9 million.

The last crop progress report published by USDA for the season placed beltwide harvesting by November 23 at 79 percent complete, one percentage point below the five-year average. In Texas, 70 percent of the crop had been gathered, versus the 74-percent average for that state.

Meanwhile, reports of physical business remained largely confined to modest quantities to meet mills’ nearby requirements, with Brazilian cotton still the primary choice across much of the cotton consuming world. Many spinners reported poor downstream demand and persistently weak yarn returns, thus few were willing to commit to purchases further ahead. In markets such as Bangladesh and Turkey, additional problems associated with high costs and difficulties accessing finance made matters worse.

Nonetheless, piecemeal enquiries were reported predominantly for Brazilian and West African lots in Bangladesh, and for Brazilian and US cotton in Turkey. Business in Vietnam picked up slightly towards the end of November, with sales noted for machine-picked supplies. In Pakistan, the expectation that mills would turn to the international market as availability of the local crop declined had so far failed to materialise, with only modest quantities from various origins changing hands.

The January contract on China’s Zhengzhou cotton futures platform rose by 70 yuan overall in November, closing the month at 13,705 yuan per tonne. Picking was completed across Xinjiang, and over four million tonnes of lint had been inspected from a total of 995 ginners in the region, according to data from the China National Cotton Exchange.

Picking concluded in Pakistan, although seed cotton deliveries were expected to continue in the coming weeks as growers release remaining supplies gradually with the aim of maximising their returns. Arrivals by November 15 amounted to 4.86 million lint equivalent bales according to PCGA, representing a decline of one percent compared to the same date last year.

Arrivals accelerated in India, but Cotton Corporation of India procurement operations for the 2025/26 crop remained slow as substantial volumes had high moisture content owing to late season rains. Auctions of 2024/25-crop supplies continued, although the volumes purchased each day were relatively modest.

The Cotton Association of India published its first estimates for the 2025/26 campaign, placing production at 30.5 million 170-kilo bales (down 740,000 from 2024/25) and consumption at 30.0 million (1.4 million lower than the figure for last season). The projection for exports was 1.7 million bales, while imports were forecast at 4.5 million.

In the Southern Hemisphere, ginning progressed in Brazil while growers prepared for the upcoming planting window. It was thought that some area may be diverted to alternative crops in view of rising production costs and persistently weak cotton prices. In Argentina, a reduction of area may also be in prospect, although the eventual total will depend in part on the receipt of sufficient moisture in the coming weeks. Sowing was meanwhile complete across Australia and stands were said to be progressing well so far.

Cotton Outlook’s forecast of world raw cotton production in 2025/26 was reduced by 145,000 tonnes in November, principally as a result of lower figures for India, the African Franc Zone and Turkey, which were partially offset by an addition for the United States. A modest adjustment was made to 2024/25.

For consumption, our figure for the current campaign was lowered by 333,000 tonnes, reflecting declines in the prospects for several major destinations. Our estimate for last season is reduced by 50,000, attributed to Bangladesh and Vietnam.

Therefore, the margin by which output is estimated to have exceeded consumption in 2024/25 widened further to 880,000 tonnes, whilst the projected surplus for 2025/26 increased to 526,000.