June 2025 Market Summary

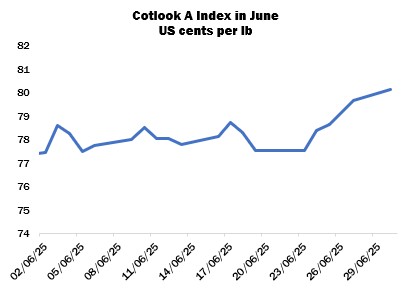

International cotton prices, as measured by the Cotlook A Index, were little altered for the first few weeks of June, but advanced steadily toward the end of the month to gain 290 cent points overall. A Forward Index (representing the price of cotton for shipment no earlier than October 2025) was introduced on June 9, at 79.95 cents per lb, 195 cent points higher than the Current Index. However, by June 30, the premium for the Forward Index had fallen to 100 points. This year’s Forward Index was introduced eight weeks later than the equivalent value last season, as merchants’ offers for 2025/26-crop cotton have been slow to emerge in view of the acutely uncertain environment faced by both the trading and spinning sectors.

In New York, the December contract advanced to 69.32 cents per lb on June 27, its highest settlement since May 6, before falling back slightly in the last session under review, for an overall monthly gain of 38 points.

As the July-9 expiry date for Washington’s 90-day pause on ‘reciprocal’ tariffs loomed, many market participants adhered to a cautious approach to business, unwilling to make commitments beyond their most imminent requirements before a greater degree of clarity and certainty on the cost of trade with the US could be gained. Negotiations with various countries that were threatened with substantial duties took place, although reports indicated disagreements on key points in several cases. Meanwhile, a separate 90-day reduction of duties between Beijing and Washington (to 30 percent on imports of Chinese products to the US, and to 10 percent on goods travelling in the other direction) is due to expire on August 12.

Nevertheless, some mill buyers secured supplies, mostly those available for nearby shipment, during price dips in June. Chinese buyers issued enquiry for Brazilian, albeit often at prohibitively low basis levels, while Bangladesh continued to show interest in West African and Brazilian cotton, price permitting. Some demand from India was also noted, and sales at the Cotton Corporation of India’s e-auctions accelerated toward the end of the period as floor prices were lowered, rendering the stocks offered by the Corporation cheaper than equivalent supplies available on the open market. In Vietnam, though, activity slowed as the arrival of the traditional ‘off season’ coincided with tariff uncertainty, so operating rates declined in many enterprises.

In Pakistan, spinners tended to focus on local new crop cotton as arrivals picked up, while reports that an 18-percent sales tax may be imposed on raw cotton imports to match that on local cotton sales (and yarn imports as announced in the federal budget in early June) led to some caution amongst buyers.

Prices on China’s Zhengzhou cotton futures platform advanced overall: the September delivery gained 545 yuan to close on June 30 at 13,815 yuan per tonne, its highest settlement since mid-March. Plants in Xinjiang were in the squaring or flowering stages by the end of the period in view, under generally beneficial weather conditions.

In its June supply and demand report, USDA reduced its domestic production forecast for 2025/26 to 14.0 million bales following extensive rainfall and delayed planting in the Delta. Some observers predicted considerably lower output as a result of the poor conditions.

However, the Acreage report released on June 30 indicated a total planted area of 10.12 million acres, higher than many observers had anticipated and above the 9.87 million acres put forward in March’s prospective plantings report. Nevertheless, the figure represents a decline of 1.06 million acres from last year. The figure for Texas was 5.73 million acres, compared to 5.98 million in 2024, but weather conditions in the coming months will of course be crucial in determining yields and abandonment and therefore the eventual output.

Crop progress reports indicated that planting was 95 percent complete by June 29, compared to the five-year average of 98 percent, while squaring was reported at 40 percent and boll setting at nine percent. By the same date, 51 percent of stands beltwide were rated good to excellent, while 32 percent were considered fair, and 17 percent were poor to very poor.

Planting in Pakistan approached a conclusion, although the area sown had fallen short of initial targets, particularly in Sindh where persistent water shortages prevented field work. Early new crop arrivals were said to be of good quality, and were met by consistent demand from domestic mills.

In India, data from the Ministry of Agriculture & Farmers Welfare indicated that sowing was complete on almost 1.4 million hectares as of June 20, ahead of the figure reported last year, although regional numbers differed slightly. The Southwest Monsoon stalled for a period in mid-June before resuming its advance to cover the entirety of the country by the end of the month. Rainfall across India was nine percent ahead of the Long Period Average by June 30 according to the Meteorological Department.

In the Southern Hemisphere, meanwhile, early picking continued in Brazil, under good weather. ANEA, the exporters’ association, increased its 2025 production estimate to 3.915 million tonnes. Near-ideal conditions facilitated field work in Australia, and harvesting was all but complete by the end of the month. Picking in Argentina progressed gradually, interrupted by persistent rainfall. Output estimates were revised lower by some observers.

Cotton Outlook’s assessment of world raw cotton output in the current season was subject to a modest revision in June, while consumption was raised by 362,000 tonnes to 24.96 million, owing to higher figures for China, Vietnam, Bangladesh and others. Therefore, the margin by which production is expected to exceed consumption has fallen to 1.09 million tonnes.

For 2025/26, our output forecast was increased to 25.97 million tonnes, as a considerable upward adjustment for China was partially offset by a lower figure for the United States. Consumption was raised by a greater margin, to just under 24.8 million tonnes, mostly attributed to China and Vietnam. If realised, the result would be an addition to global stocks of 1,173,000 tonnes by the end of the next marketing year.