July 2025 Market Summary

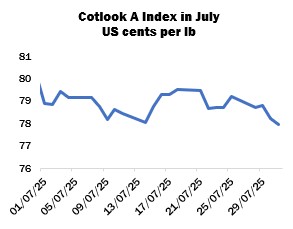

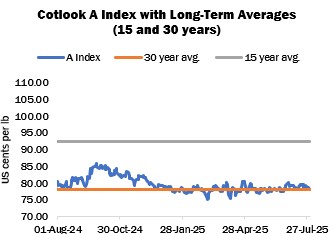

International cotton prices, as measured by the Cotlook A Index, fell by 220 cent points overall last month. July 31 also marks the last day of the current season, and the expiry of the 2024/25 A Index. The final value of 77.95 cents per lb compares to a high of 85.80 attained on September 25, 2024. A low of 74.95 was recorded on March 5 this year while the average for the 12-month period was 79.61 cents per lb.

From August 1, the 2025/26 A Index (henceforth the Current Index) will stand alone until after the year-end, when a new Forward (2026/27) A Index will be introduced as soon as sufficient market evidence is available.

In New York, the December contract remained range-bound, settling within a margin of just 155 cent points, eventually closing the period at 67.25 cents per lb (down 88 points).

Much like in previous months this year, July was dominated by discussions regarding US tariffs. Uncertainty prevailed as the July-9 expiry date for the pause on ‘reciprocal’ tariffs on most countries was extended until August 1, while negotiations with China continued on a separate track, with a 90-day reduction of duties set to end on August 12. Talks between Washington and Beijing in Stockholm at the end of the month had not yet reached a conclusion, but reports suggested a further 90-day extension was likely.

Meanwhile for India, a top supplier of cotton products to the US, an import tariff of 25 percent was announced for goods entering the latter country according to a social media post by the US president on July 30, just one percentage point below the levy initially proposed. An unspecified additional “penalty” associated with India’s trade with Russia was also suggested.

On the eve of the deadline, negotiations were still taking place with countries including Pakistan and Bangladesh, with new rates (set to take effect from August 8) eventually emerging of 19 and 20 percent, respectively. In Bangladesh, it was understood that offers to buy US goods including cotton had been put forward in talks between the nations, although confirmation was awaited.

Other tariffs set as the August 1 deadline expired included 20 percent for Vietnam, 19 percent for Indonesia, and 15 percent for Japan, South Korea, the European Union and Turkey.

Mill buying remained largely sporadic and hand-to-mouth in nature, as few spinners were willing to add to their inventories while uncertainties regarding international trade and tariffs persisted. Interest from Bangladesh continued for nearby or afloat supplies, but many mills still face issues generating Letters of Credit, while the lack of clarity discouraged purchases further ahead. Buyers in Vietnam secured relatively modest volumes of machine-picked cotton available nearby during price dips to cover gaps in requirements. Import enquiry was also noted from India, while active purchases of local cotton continued at the Cotton Corporation of India’s e-auctions.

In Pakistan, news at the end of the month confirmed that the earlier announced 18-percent tax on imports of cotton, cotton yarn, and cloth (refundable when final products are exported, as already applicable to sales of local supplies) will finally be implemented. The announcement was welcomed by many in the sector as levelling the playing field between local and imported materials. Some organisations criticised the delay, though, for creating uncertainty at a key time as domestic growers harvest and market the new crop. The change may slow import business further, but mills were already predominantly focused on procuring local new crop arrivals.

Following an extended period on the sidelines, Chinese buyers took the opportunity afforded by the wide differential between ZCE and ICE futures to book new business, mostly comprising Brazilian supplies at low basis levels as well as some Australian.

The widening premium of ZCE over ICE was largely the result of a two-month rally on the former platform (while the lead ICE contract remained range bound). The increase was attributed to the prospect of a tightening supply in China following figures published last month that revealed stronger than expected consumption throughout the season thus far, while raw cotton imports dwindled, reducing the stocks available to the market ahead of local new crop arrivals.

However, the ZCE September contract began to reverse course after reaching a high of 14,300 yuan per tonne on July 18, eventually ending the month 115 yuan lower, at 13,700 yuan per tonne, nonetheless still representing a premium of almost 20 cent points over the December contract in New York.

Meanwhile, stands across Xinjiang were flowering, and overall plant development was faster than a year earlier. However, hot weather resulted in concerns for yields in some parts, although irrigation should mitigate the impact to an extent, while pest infestations were being monitored in fields that had received persistent rains.

The US Department of Agriculture’s July supply and demand report included an increase to its domestic output forecast for 2025/26, to 14.6 million bales, based on greater planted and harvested area figures, although some observers anticipate lower planting figures than those currently put forward by USDA (10.12 million acres). Beginning stocks were meanwhile reduced by 300,000 bales, while ending stocks rose by the same margin.

Crop progress reports indicated that squaring stood at 80 percent by July 27, behind the 83 percent five-year average. Boll setting was reported at 44 percent by the same date, compared to the 46 percent average. Beltwide, conditions improved slightly overall: 55 percent of stands were rated good to excellent (up four points from the end of June), while 31 percent were considered fair (down one point), and 14 percent were poor to very poor (down three points).

Elsewhere, harvesting picked up in Pakistan, although the first PCGA arrivals report for the season indicated that deliveries by July 15 amounted to 297,750 tonnes, 33 percent below the figure recorded by the same date last year, as a shortfall in Sindh more than offset an increase for Punjab. Persistent rainfall earlier in the month was generally considered beneficial, but some earlier sown fields experienced increased pest infestations.

In India, data from the Ministry of Agriculture & Farmers Welfare showed that 10.3 million hectares had been sown by July 25, versus the 10.5 million ha recorded by the same date in 2024. Progress varied across regions, and work in Gujarat was 13 percent behind last year’s pace.

In the Southern Hemisphere, picking advanced in Brazil, though work lagged behind last year’s pace in Mato Grosso. Early results were positive overall, but yields were said to be mixed in Bahia. Nevertheless, CONAB raised its forecast of 2025 production to 3.94 million tonnes. Clear weather allowed picking to approach a conclusion in Argentina, although the unhelpful conditions throughout the growing season have resulted in varied yields. Harvesting finished in Australia and processing continued to advance. A considerable proportion of the crop was understood to comprise lower grade supplies.

Cotton Outlook’s forecast of world raw cotton output in 2025/26 was increased to 26.09 million tonnes in July, as higher figures for the US, Australia, and smaller producing countries were only partially offset by a reduction for India. Several adjustments informed the change to our consumption estimate, which was 15,000 tonnes higher than the previous month. Thus, the margin by which production is expected to exceeded consumption widened to 1,275,000 tonnes.

For the concluded 2024/25 season, world output was raised by 113,000 tonnes, to 26.16 million, attributed largely to an addition for India, while global consumption was subject to a modest upward revision, to 24.97 million tonnes. Therefore, the estimated surplus for that season is larger than the figure put forward in June, at 1,188,000 tonnes.