January 2026 Market Summary

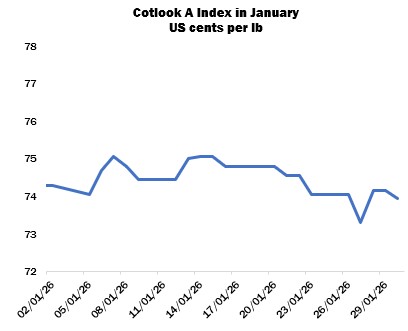

International cotton prices as measured by the Cotlook A Index declined modestly overall in January, ending the month at 73.95 cents per lb. In New York, the March delivery fell by 110 cent points to settle at 63.17 cents per lb, having recorded a new life of contract low close on January 26 of 62.97 cents. An increase in the basis of shippers’ offers, particularly for Brazilian cotton, was observed, as well as shifts from quotes being based on the March delivery to May. Meanwhile, daily volumes were robust, and open interest climbed consistently throughout the month to reach 373,415 contracts, a gain of around 70,000 contracts since the end of December and a new record high.

The pace of raw cotton import purchasing improved in most quarters in January, particularly in the first half of the month. Buyers in China were active, encouraged by the wide ZCE/ICE spread as well as the allocation of Tariff-Rated Quota, securing lint from Brazil and the US among other origins. Yarn demand from China also picked up for both domestic and international supplies, buoying prices and improving prospects slightly for spinners in major manufacturing hubs, which perhaps boosted additional raw material replenishment.

Buyers in Pakistan turned to the international market as local supplies dwindled, securing attractively priced lots and recaps from various origins to cover mostly against second quarter requirements. Interest also persisted in India despite the resumption of the 11-percent tariff on imports at the turn of the year, as domestic cotton prices were significantly higher in comparison.

In Bangladesh, sporadic demand continued for African and Brazilian lots, but some took a more cautious approach in the run up to the general election planned for February 12, with work expected to be disrupted for a few days. Furthermore, BTMA threatened on behalf of its members to suspend all spinning operations from February 1 if the government did not implement the withdrawal of duty-free facilities for imported yarns, a move strongly opposed by manufacturers and exporters but considered necessary by mills who have struggled to compete. That threat was withdrawn as assurances were made by the government, but the outcome of talks between key stakeholders was still awaited.

Meanwhile, the Buying American Cotton Act was introduced to Congress in the United States, marking the first step in the legislative process. While there is currently no indication of the timeline for its approval and implementation, observers noted that it would likely prove beneficial for domestic cotton demand.

US upland export commitments in the three weeks to January 22 rose by a net 955,800 running bales, boosted by two consecutive marketing-year highs before a slight drop off. For the first time since September, Vietnam was not the primary destination in the third report, having been overtaken by Pakistan for that week. The additions brought the running total of commitments to all destinations to 7,553,500 bales, still behind the 8.7 million recorded by the corresponding moment in 2024. Upland shipments climbed steadily in the weeks under review, reaching a MY high in the third report. Cumulative exports therefore increased to 3,587,300 bales, versus 3.46 million last year.

USDA made a downward revision to its US cotton output estimate in its January supply and demand report, to 13.92 million bales versus 14.27 million in December. The adjustment was attributed mostly to a lower figure for the Memphis Territory, partially offset by increases elsewhere. Beginning stocks, domestic use and exports were all unchanged, so ending stocks were reduced to 4.2 million compared to 4.5 million a month earlier.

The estimate for global production was also cut, by more than 350,000 bales to 119.43 million, as an addition of one million bales for China was outweighed by reductions for India, the US, Argentina and Turkey. On the other hand, worldwide exports and consumption were raised to 43.77 million and 118.92 million, respectively. Beginning stocks were adjusted lower, and ending stocks were cut to 74.48 million versus 75.97 million in December.

In China, the May contract on the Zhengzhou cotton futures platform increased by a further 220 yuan overall in January, to close at 14,770 yuan per tonne, having reached a new contract high settlement of 14,965 on January 7.

According to data from the China National Cotton Exchange, over 7.1 million tonnes of lint had been inspected in Xinjiang by the end of the month, from a total of 1,018 ginners in the region. Progress stood 13 percent ahead of the same moment a year earlier.

Daily arrivals slowed in India, in line with seasonal patterns. The Cotton Corporation of India had procured around 4.4 million tonnes of 2025/26 crop seed cotton by the end of the month, equivalent to perhaps 30 percent of the total expected output. Auctions of supplies from the current campaign began on January 19, and over 300,000 bales were sold in the first two weeks.

In the Southern Hemisphere, planting accelerated in Brazil with work placed at 61 percent complete nationwide by January 24, according to CONAB. Safra (first crop) cotton was said to be developing well so far, although growers in Mato Grosso were alert to the possibility of pest infestations following wet weather. Production estimates in Australia were maintained at around one million tonnes, significantly lower than the last campaign, in view of a smaller planted area and reduced water availability in many parts.

Cotton Outlook’s forecast of global raw cotton output in 2025/26 was reduced modestly in January, as higher figures for India, China, and the US were more than offset by adjustments for the African Franc Zone, Brazil, and others.

For consumption, our assessment for the current campaign was raised by 120,000 tonnes, primarily reflecting increases in the prospects for China, India and other countries, but declines for Bangladesh, Brazil and Indonesia.

Therefore, the margin by which production is projected to exceed consumption in 2025/26 has narrowed to 841,000 tonnes, down from 970,000 in late December.

Our initial forecasts for the 2026/27 season will be published at the end of February.