February 2026 Market Summary

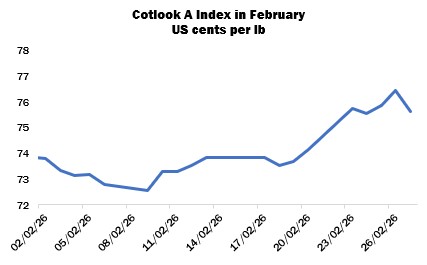

International cotton prices as measured by the Cotlook A Index advanced in February, ending the month at 75.65 cents per lb, an increase of 170 cent points overall. The A Index recorded its firmest value since early November late in the period before falling back somewhat. In New York, the May delivery rose by 68 cent points to settle at 65.61 cents per lb. Meanwhile, volumes were boosted by fund rolls, and open interest declined from its recent record high.

A slightly slower pace of import demand was witnessed in February, owing in large part to holiday observations across much of the world, including Lunar New Year and Ramadan. That said, sporadic business was still reported, particularly from those mills with nearby requirements to fill.

In Bangladesh, focus remained largely on African and Brazilian supplies, while US lots were also under discussion in light of a trade agreement announced by Dhaka and Washington, which included duty-free access for Bangladeshi textiles and apparel made with US cotton to that market. The smooth passage of the election in Bangladesh on February 12 was also met with relief and a hope that improved business confidence could be encouraged going forward.

An accord between India and the US was also declared early in the month under review, which proposed to cut ‘reciprocal’ levies on Indian goods from 25 percent to 18, while an additional 25-percent duty related to India’s purchases of Russian oil was scrapped. India committed to reducing trade barriers for US goods and increasing imports in return. Companies in Indonesia meanwhile signed a deal to purchase 93,000 tonnes of US cotton over an unspecified period.

Some exporters in Pakistan were concerned that market share could be lost if a trade deal similar to those made by its neighbours with the US could not be secured. Mill buyers here continued to purchase recaps and other attractively priced supplies from the international market as local availability declined.

The US Supreme Court ruled on February 20 that the President did not have authorisation under the International Emergency Economic Powers Act (IEEPA) to impose tariffs without congressional approval, thus striking down the ‘reciprocal’ duties applied on many countries last year. The adminsitration declared it would instead implement temporary blanket tariffs of 10 percent under different legal provisions. It is so far unclear if and how refunds might be issued for levies already paid by US companies, or how the ruling will affect trade deals agreed with various nations in the preceding weeks and months.

The results of the US National Cotton Council’s Planting Intentions survey were released on February 12, indicating a reduction in beltwide area in 2026 of 3.2 percent to nine million acres, suggesting a possible output of 12.7 million bales, which would be the smallest crop since 2015/16 if realised.

USDA meanwhile published its first forecasts for 2026/27 on February 19, indicating only a slight decrease for domestic production (13.6 million bales versus 13.92 in the current campaign), based on a planted area of 9.4 million acres (9.28 million last year), abandonment of 18.8 percent and an average yield of 856 lbs per acre. Global output is also expected to decline according to the Department, while the figure for consumption was increased. Thus, ending stocks were placed at 71.2 million bales compared to 75.1 million this year.

In China, the May contract on the Zhengzhou cotton futures platform ended the month 560 yuan higher at 15,330 yuan per tonne. Strong gains were recorded following the return from the Lunar New Year holiday, resulting in a new contract high settlement for May of 15,450 yuan per tonne on February 26. The rally perhaps reflected the bullish movements in New York, and was likely also motivated by reports of robust consumer spending over the holiday period.

Inspections of lint in Xinjiang had reached almost 7.38 million tonnes by the end of February, over one million tonnes more than the same date a year earlier, and approaching BCO’s estimate of output for the region of 7.417 million tonnes.

The Cotton Corporation of India had procured around a third of the total expected output for the 2025/26 campaign by late February. Sales were relatively modest until the end of the month, when business was encouraged by a notable price reduction.

Meanwhile in Pakistan, planting commenced in parts of lower Sindh and pockets of Punjab as temperatures picked up. The provincial government in the latter region targeted 700,000 acres for early sowing.

In the Southern Hemisphere, planting was all but complete in Brazil by the end of the month, in line with last year’s pace. Initial picking was under way in Argentina under generally favourable conditions, while harvesting also began in Australia. Early field reports were positive.

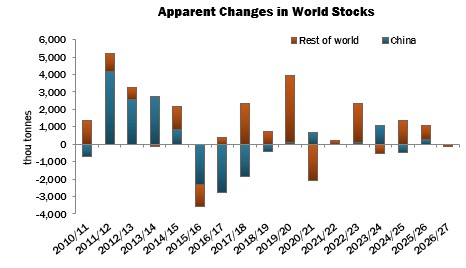

Cotton Outlook’s first estimates for 2026/27 place global raw cotton production at 25.08 million tonnes (a decline of four percent from 2025/26), and consumption at 25.23 million tonnes (up by 0.5 percent). The result would be a reduction of global stocks by the end of the next marketing year, of 146,000 tonnes.

Declines in output are forecast for most of the major producers, although larger crops are anticipated in India, the African Franc Zone and some smaller producing countries.

Consumption is projected moderately higher, in view of relatively resilient global growth forecasts and encouraging textile and garment trade data from several quarters. With that said, uncertainty still persists regarding changing tariffs and the potential impacts on commerce and costs.