August 2025 Market Summary

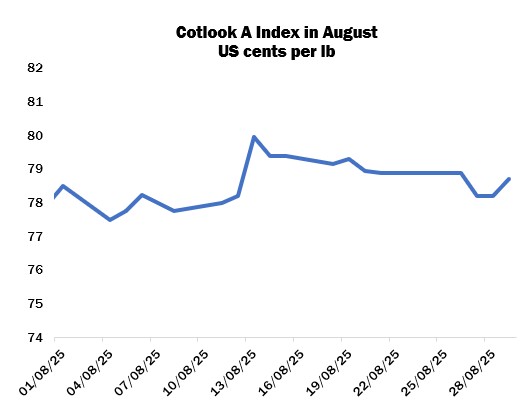

International cotton prices, as measured by the Cotlook A Index firmed by 75 points on balance in August, to be placed on the last day in view at 78.7 cents per lb. In New York, the December contract settled within a range of just 203 cent points, closing at a peak of 68.39 cents per lb on August 12 as traders reacted to the latest USDA supply and demand report (detailed below), before falling back to eventually end the month 71 points lower overall at 66.54 cents per lb.

Meanwhile, Beijing and Washington agreed on August 11 to further extend the pause on higher duties until November 10, to allow time for additional trade negotiations. A levy of 30 percent will remain on Chinese products imported to the US, and of ten percent on trade in the opposite direction.

India declared a pause on import tariffs for raw cotton until December 31, a decision intended to support local spinners and manufacturers following the imposition of 50-percent duties on Indian goods entering the US (including a 25-percent penalty associated with that country’s trade with Russia), a key market for India’s textiles and apparel exports.

In light of the announcement in New Delhi, import demand from Indian mills picked up slightly, especially when New York futures dipped below 67.00 cents per lb. Spinners in Pakistan were largely focused on the domestic crop, although some business was confirmed for international supplies from various origins. Interest from Turkey was noted towards the end of the period, mostly for Brazilian and US cotton, as mills expect prices for domestic cotton to remain higher than many are willing to accept. However, conditions in that country’s spinning and manufacturing sector continued to be described as extremely difficult.

Exporters of textiles and garments to the US in Bangladesh and Vietnam were hopeful that the higher tariffs placed on competitors, most notably India, as well as the uncertainty regarding duties on China, would result in orders shifting in their direction. Reports from local observers, particularly in the former country, indicate an uptick in business already. In addition, a greater level of interest in US cotton has been noted, as manufacturers position themselves to achieve tariff reductions on goods containing US materials when the Buying American Cotton Act comes into force.

On August 25, China’s National Development and Reform Commission announced an allocation of 200,000 tonnes of Sliding-Scale quota for 2025. All the quota must be applied against processing trade imports, for use in goods destined for export only. Following the announcement, a slight uptick in enquiry was witnessed, largely for machine-picked supplies for delivery before the end of the year.

Prices on China’s Zhengzhou cotton futures platform rose modestly overall in August. The September contract gained 95 yuan to close the month at 13,795 yuan per tonne. Meanwhile, plants in Xinjiang continued to develop well overall and boll opening increased. Picking is expected to begin in September.

In its August supply and demand report, the US Department of Agriculture reduced its domestic output forecast for 2025/26 to 13.21 million bales, down from 14.6 million put forward in the previous report, primarily as a result of more modest area figures than previously envisaged. Exports were also lowered while consumption was unchanged, with the result that the estimate for ending stocks was reduced by one million bales, to 3.6 million.

According to crop progress reports, 81 percent of stands beltwide were setting bolls by August 24, and 20 percent of bolls were opening, both figures slightly behind the five-year averages. Fifty-four percent of plants were judged to be in good or excellent condition (down one point from the end of July), while 33 percent were considered fair (up two points), and 13 percent were poor to very poor (down one point).

Meanwhile, additional rainfall in Pakistan raised concerns of flooding and pest infestations, but stands nonetheless continued to develop well overall. Arrivals by August 15 were placed at 887,400 tonnes by the PCGA, 17 percent lower than the figure recorded by the same date last year, although it is thought that a considerable proportion of business is being conducted outside of official channels, and are therefore not included in PCGA reports. Meanwhile, some fields were planted later than usual, resulting in slower deliveries.

Sowing in India had reached 10.85 million hectares by August 25 according to the Ministry of Agriculture & Farmers Welfare, around 2.6 percent behind the figure recorded by the same moment a year earlier. Modest quantities of new crop arrivals began, while remnants of the 2024/25 crop also continued to arrive at gin yards.

In the Southern Hemisphere, harvesting accelerated in Brazil’s major Mato Grosso state, but work remained behind last year’s pace after a slow start due to untimely wet weather. Some observers expressed concern that the quality composition of the crop might have been affected by the late precipitation. Across the country, work was around 60 percent complete by the end of the month. Ginning and classing operations progressed in Australia, while preparations for initial sowing began. In Argentina, picking was drawing to a close following rain-related delays, while ginning was expected to continue until September or early October.

Cotton Outlook’s forecast of global raw cotton production in 2024/25 was raised by 150,000 tonnes in August, attributed predominantly to upward revisions for India and Brazil. For 2025/26, our output forecast was lowered slightly, as increases for China and Pakistan were more than offset by reductions in the US and elsewhere.

For consumption, our estimates for 2024/25 and 2025/26 were raised by 431,000 and 531,000 tonnes, respectively, mostly on account of higher figures for China, Pakistan, India and Vietnam.

Therefore, the margin by which output is estimated to have exceeded consumption in the now concluded 2024/25 season has narrowed to 907,000 tonnes, whilst the projected surplus for 2025/26 has declined to 637,000.