September 2025 Market Summary

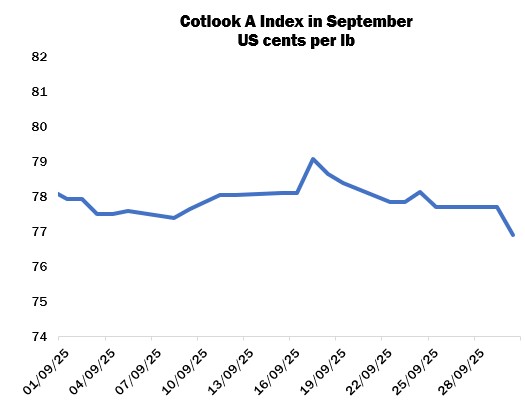

International cotton prices, as measured by the Cotlook A Index, declined by 180 cent points overall in September, to end the period at 76.9 cents per lb. In New York, the lead December contract lost 77 cent points, closing on September 30 at 65.77 cents per lb, having recorded a new life-of-contract low settlement of 65.5 cents in the previous session. Open interest meanwhile rose further, reaching 278,283 contracts on the last day of the month, its highest level since April 4.

India was one of the most active buyers earlier in the period, but activity slowed as the window to ship cotton to that country duty-free narrowed and domestic prices declined, amplified by a weaker rupee. Nonetheless, additional import business was encouraged as futures prices fell. Bangladesh continued to face banking issues, limiting the conclusion of sales, although enquiries persisted largely for West African and Brazilian lots. Mills in Pakistan remained focused on the domestic crop, but modest quantities of international supplies found buyers during the month.

Orders in Vietnam picked up somewhat as the peak season for garment manufacturing approached, but observers noted that demand was still dull overall, and some mills had already covered against their nearby cotton requirements in previous weeks.

In Turkey, asking rates for domestic lint remained above the levels many buyers were willing to contemplate, so import enquiry persisted for a range of origins, including Brazilian, US, Argentine and Greek. However, the price ideas of buyers and sellers were still often difficult to reconcile.

Prices on China’s Zhengzhou cotton futures platform declined overall in September. The January contract fell by 1,015 yuan to end the month at 13,245 yuan per tonne, its weakest level since May. Meanwhile, the Xinjiang crop continued to mature, and picking began in some fields.

The US Department of Agriculture published its latest supply and demand report, which featured only a 10,000-bale addition to the domestic output forecast, to 13.22 million bales. Meanwhile, updates to USDA’s global balance sheet included higher production, consumption, and exports, resulting in a reduction of world ending stocks to 73.1 million bales, the lowest in four years.

Across the US cotton belt, boll openings were reported at 67 percent by September 28, slightly below the average. The condition of the crop declined slightly: 47 percent of plants were judged to be in good or excellent condition (down seven points from the end of August), while 36 percent were considered fair (up three points), and 17 percent were poor to very poor (up four). Nonetheless, the proportion of stands rated good or excellent remained greater than at the same point in the past few seasons. Harvesting was 16 percent complete, on par with the average but three points behind last year’s pace.

Fair weather returned in Pakistan, allowing harvesting to accelerate again. While floods resulted in damage to fields, infrastructure, and livelihoods in southern Punjab, cotton fared slightly better than other crops and inundations in Sindh were largely avoided. According to PCGA, arrivals by the end of September totalled 3.04 million lint equivalent bales, an increase of 1.7 million bales from August 31, representing a rise of 49 percent from the comparable figure a year earlier. Some local observers, however, expect deliveries to slow in the coming weeks, and a final output below last year’s total.

New crop deliveries in India also picked up as the month progressed, although forecasts of heavy rains in October raised concerns of damage to open cotton. Seed cotton procurement operations by the Cotton Corporation of India officially begin on October 1, the first day of the Indian cotton season, and commentators noted that substantial purchases may again be anticipated, as a result of a higher MSP and relatively low domestic values.

In the Southern Hemisphere, meanwhile, picking had drawn to a close in Brazil and ginning continued to progress. The output estimates of several organisations and observers were increased to over four million tonnes. Attention subsequently turned to planting prospects for the next crop, and some commentators noted the possibility of a smaller area dedicated to cotton, considering rising costs and low lint prices, although competing crops are also facing similar challenges. Early planting commenced in parts of Argentina, but area is expected to fall short of last year’s total. Sowing also expanded in Australia’s Queensland state. Weather forecasts indicated above-average rainfall in the east of the country over the coming months, which would further replenish water storage levels.

Cotton Outlook’s forecast of world raw cotton output in 2025/26 was lowered by 82,000 tonnes in September, to just under 25.9 million, as additions for China, India, and the United States were more than offset by reductions in various other countries. A modest upward adjustment was made to the 2024/25 estimate overall.

Our consumption figures for both seasons were raised, by 162,000 in 2024/25 and just 32,000 in the current campaign, largely attributed to increases for China in each case.

Thus, the margin by which output is estimated to have exceeded consumption last season has narrowed to 772,000 tonnes, whilst the projected surplus for 2025/26 has declined to 523,000.